October Option Strategies

October Option Strategies

Fujisan here.

I’m running out of my Ukiyo-e posting and I’m switching my opening theme into tropical islands. I hope you guys like it.

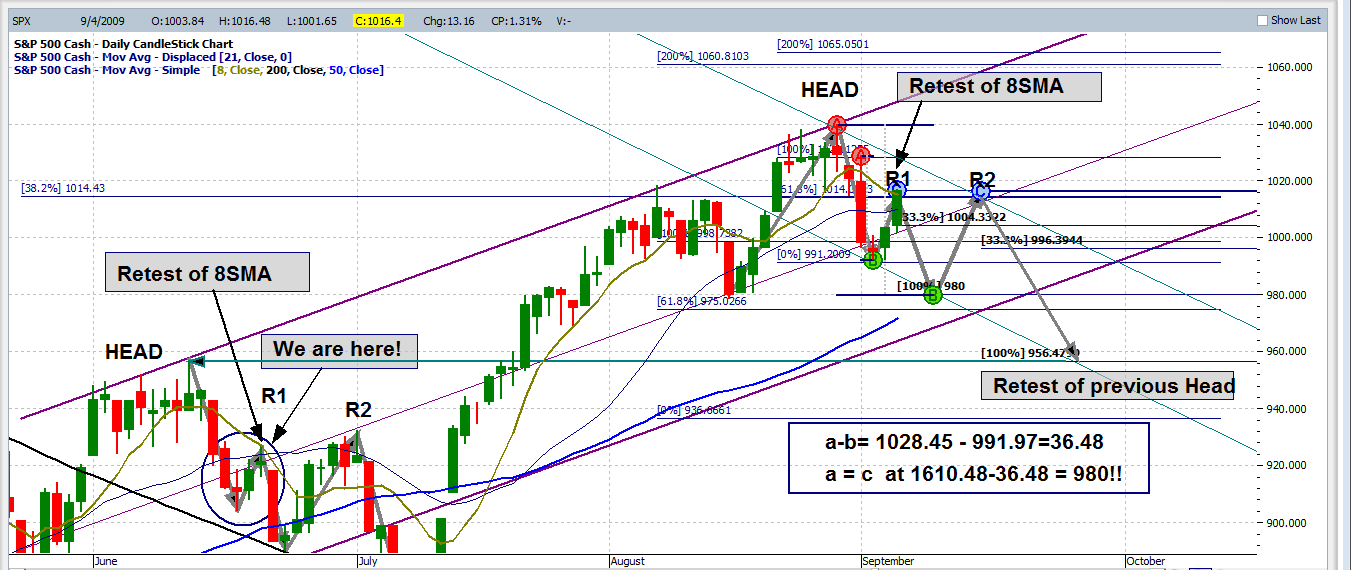

SPY Roadmap – Medium Term

I see many of you have loaded Dec & Mar OTM put options and I would like to point out a couple of things before you load up more OTM put options.

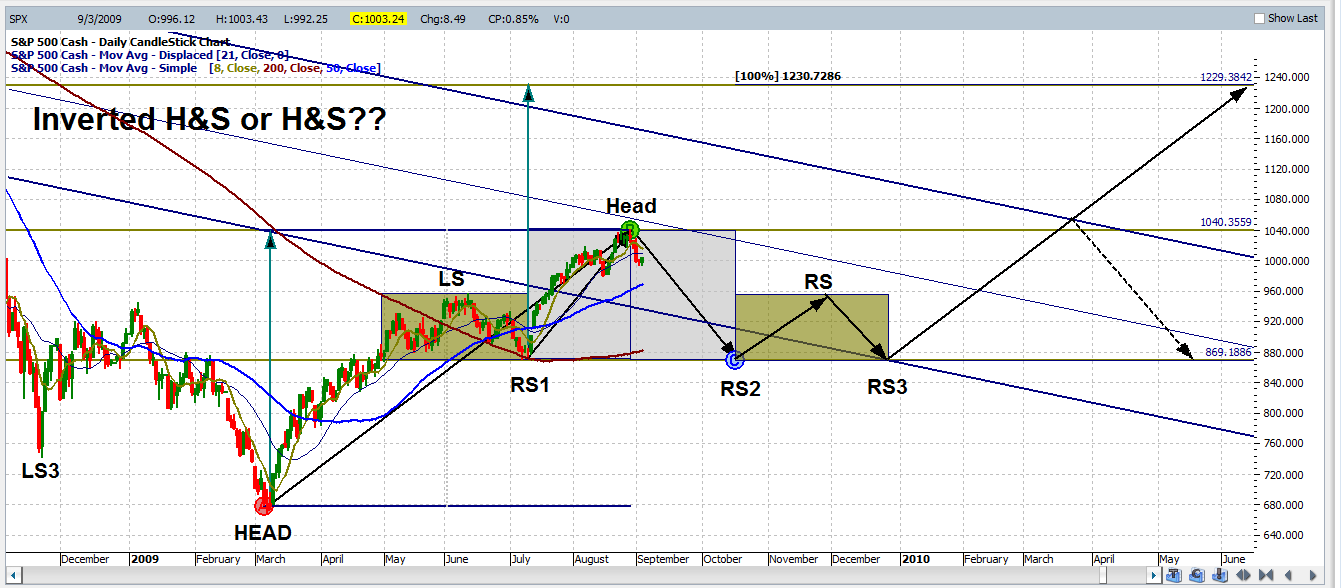

Inverted H&S Scenario

Here is my SPY road map for a medium term. Although I’m short term bearish, I’m not as entirely bearish as you guys and I’m expecing a possible leg up toward the end of the year if inverted H&S pattern works out. This is the best “guess” scenario based on the current pricing pattern.

H&S Scenario

Now, here is the “notorious” H&S pattern that failed last time. I measured the same time frame to form the right side of the head and the right shoulder (although the downside is much faster than the upside (it’s about 2 to 3 ratio) – but I love symmetry and the right side – left side match so I decided to use the same time and price ratio to come up with this price projection).

Again, it may not even form another H&S pattern here, but for the discussion purposes, I’m going to use this pattern for the October price projection.

As you can see, SPY may possibly be sitting around $87 area in December (if all works out) and here is SPY Dec open interests. I always like to look at the open interests and see how the market participants look at the overall market direction, and it has served me quite well in the past. You see pretty good open interests at 80, 82, 85, 90, and 95, and it’s not excessively bearish.

Now, let’s say that you have Dec 70 put options, and SPY drops down to $87 in October. What would happen to your Dec options?

Note: The below price analysis is based on Thursday close (I wrote this up on Thurs night) so it’s not reflected by the Friday close therefore you won’t be able to duplicate the same PL chart.

December 70 Naked Put Options

If everything stays equal, you may be able to make $230 over your $470 investment if SPY goes to $87 in October, but please note that the probabilities of SPY “touching” $87 by Oct and OPX is only 12% and the odds are clearly against you.

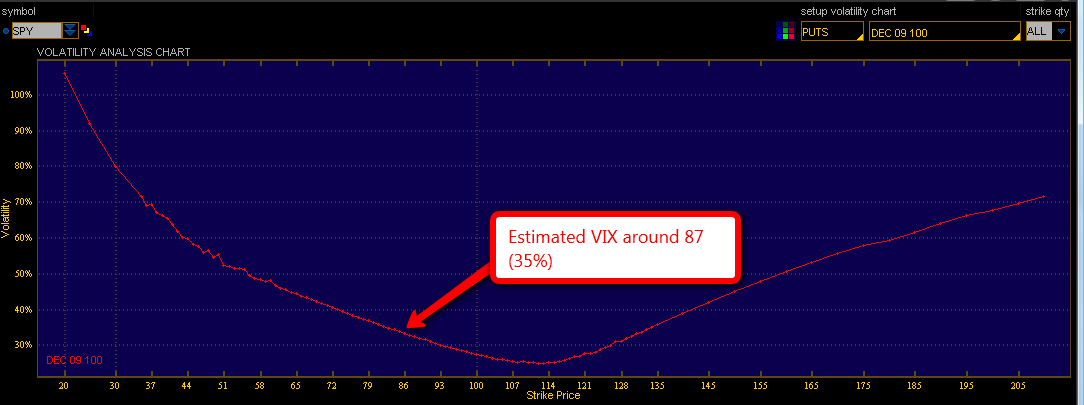

Now, of course if SPY drops down to $87, VIX will spike up and inflate your put options, but how high would it go up?

Here is Dec 100 Put Option volatility study. Based on this graph, estimated VIX at the price of $87 would be around 35%. Similarly, I looked up the historical VIX at $87 on April 30 and July 8th and they were 36.5 and 31.3, respectively, so we could make a pretty good estimate of VIX to be around 35% if SPY hits $87.

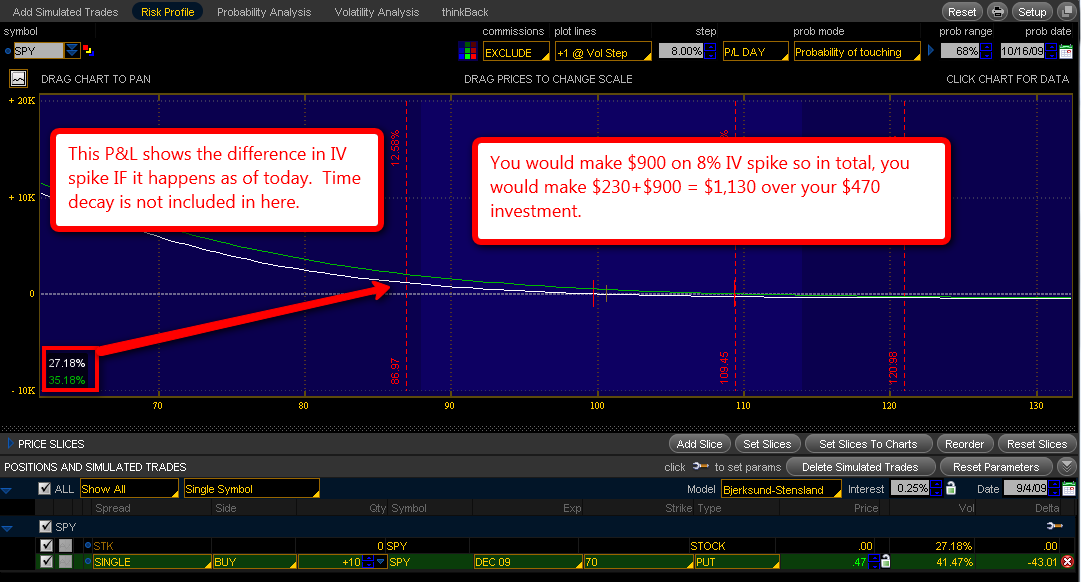

Here is how PL graph looks like if SPY drops to $87 and IV spikes to 35% as of today. I coulnd’t set it up to reflect time decay so this is just to show you how IV spike would inflate your put options as of today. In summary, you would make $330 on a price move and $900 on IV spike, $1,230 in total over your original $470 investment. This is not bad at all, but I would have to emphasize that this position is more like an IV play (you are making money mostly due to IV rush) and you are counting on the future IV spike to inflate your OTM put options.

Please also remember that the probabilities are against you and your breakeven is at $90, only a few points above the target price of $87 and there will be a constant battle between theta burn and IV crush. If you are taking this position, please make sure to put in the amount that you can afford to lose as the probability of success is only 12%.

If you still like to play with put options, please do yourself a favor and buy at least ATM options instead of OTM options.

Caution: Anyone with Dec 70 put options should close the position in October. You can hedge your position by selling options at a lower strike price, but that’s not 100% hedge and by the time it comes back down to $87 in Decmeber (after forming the right shoulder), your Dec 70 put options would be entirely worthless. Also, let me remind you that there is 88% probability that SPY may not be able to make it to $87 by Oct OPX.

Any Possible Hedging Strategies??

Mole was asking if there is any hedging strategy on these OTM put options. Unfortunately, there are not much remedies at this point. As the premium is very small to begin with, it would cost more to sell the lower strike price (to make it a vertical spread) or to create some kind of calendar/diagonal spread. You would just have to sit through it hoping that IV would pick up somewhere down the line (which it will). This is the reason why I never recommend far out of the money options.

No Exit Point

If I understand this strategy correctly, you won’t get out of this trade until it finally works out — which perfectly makes sense as you may easily lose as much as 50% of the entire premium if you have to get out of the position when the trades are against you. But from a risk management perspective, this is not really an ideal situation that you like to be in and if you do, please limit your exposure to less than 1% of your account balance.

Now, if you like to double your money without relying on the variables (such like IV spike and negative theta), there are much better ways to play this out.

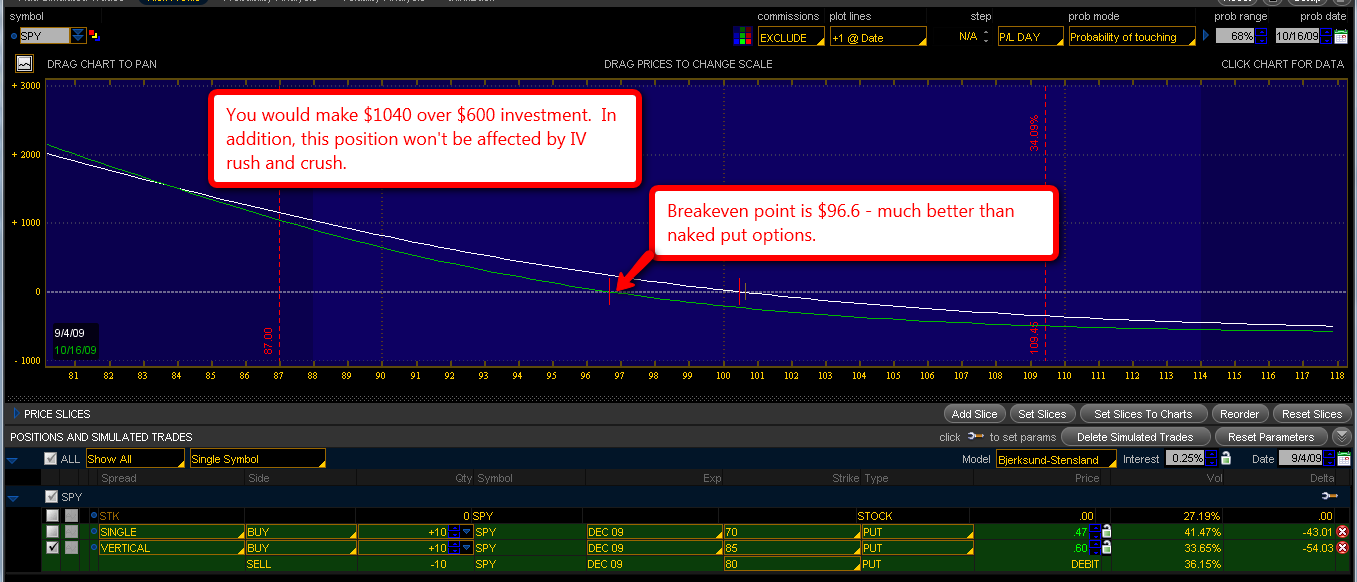

December 80/85 Put Vertical Spread

Here is Dec 80/85 put vertical spread. You buy Dec 85 put options and sell Dec 80 put options to create a vertical spread. You can make $1,050 over $600 investment, and the breakeven point is at $96.6 – much higher than Dec 70 put options of $90. As this position is still OTM spread, it has a negative theta but not affected by IV rush and crush as much as put options. You would have a much more stable account balance overtime. Probability of success is 35%.

October 105/90 Put Vertical Spread

Here is October 105/90 put vertical spread. You buy Oct 105 put options and sell 90 put options to create a vertical spread. You make $959 over $531 and this position has a positive theta. Probability of success is 49%.

As we are in the probability business, it would always be a good idea to choose the higher probability play if the payout is similar. I hope I made my case.

Summary

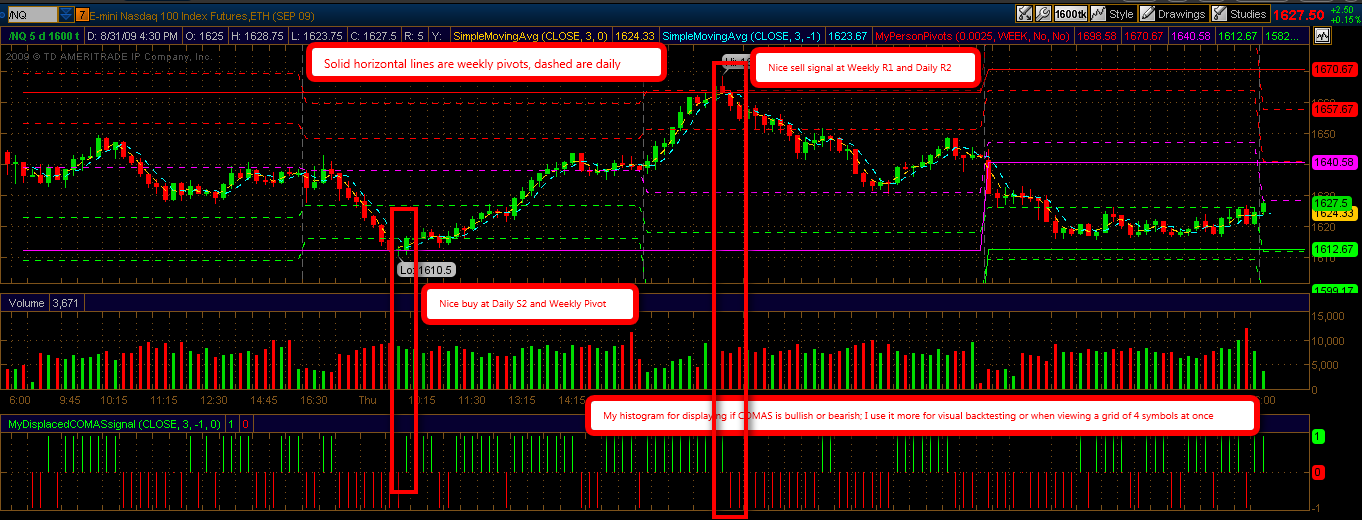

COMAS set up

Lastly, anyone using Person’s Pivot – I was able to setup COMAS at TOS, thanks to Dan Robbins. I was using other momentum indicators like stoch & RSI as a confirmation, but COMAS works much better and picks up the change of the momentum much quicker than the typical indicators.

If you are interested in setting up COMAS, here is how:

This is the direct quote from Dan’s email:

“The study is called TypicalPrice. It will plot the 1 period pivot point and which ever number you select for the 2nd period pivot point moving average.

Or, you can simply make your own by adding SimpleMovingAvg twice to your chart. Select H+L+C/3 as the price and then choose whichever number of periods you want. This is what I do. In Person’s book, he mentioned using the 1 period and 3 period for the changeover, however I like using the 3 period for both, but one is displaced forward (by using -1 in the displace setting). Lately, I’m finding a tick chart (1600 tick) works well with ES, NQ, and TF, but not for FX.

“# My version of COMAS

declare lower;

input price = close;

input length = 3;

input mydisplace = -1;

input displace = 0;

def fastAvg = Average(price[-displace], length);

def slowAvg = Average(price[-mydisplace], length);

def value = fastAvg – slowAvg;

Histogram Set Up

# Histogram Magic

def longsignal = if (Value > 0) then 1 else 0;

def shortsignal = if (Value < 0) then -1 else 0;

plot long = longsignal;

long.SetPaintingStrategy(paintingstrategy.histogram);

long.AssignValueColor(Color.Green);

plot short = shortsignal;

short.SetPaintingStrategy(paintingStrategy.HISTOGRAM);

short.AssignValueColor(Color.Red);

Thanks for your help Dan!

I hope everybody has a very nice labor day weekend.

Fujisan

Sat Update:

“Naked” simply means “not hedged”. I eliminated it so that you won’t get the wrong idea.

I also updated Histogram Set Up as suggested by Dan. Thanks again!

Sunday Update

PUBLIC ANNOUNCEMENT: I’m sorry to tell you guys about this, but I decided to quit my weekly post. This will be my last posting on this site. Thank you so much for your support and encouragement for the past 5 months. I really enjoyed it and I hope you did too. I will see you somewhere on this cyperspace. Good luck to you all!

{kind=link}

{kind=link}

{kind=link}