Let’s have fun with credit spreads!

Let’s have fun with credit spreads!

Fujisan here.

Isn’t it totally amazing that Aug OPX is coming up in a matter of two weeks?? Well, this is a wonderful time to build Aug OPX positions to take advantage of the final 2 weeks of the time decay. Summer is half way through, so let’s have fun with credit spreads!

Before I dive into “Fujisan’s” credit spreads, I will go through an example of a typical credit spread.

Typical Credit Spreads

Credit spreads are the combinaion of either call or put options with the same months with different strike prices. It’s typically a delta neutral strategy covering 1~2 standard deviations with a low return/high risk.

Here is an example of a typical credit spread. This credit spread is SPY AUG 106/108, which covers one standard deviation on the upside (68% of the price movement until OPX) and you can get rewarded with $140 ($170 – $30 commission) off of a total cost of $1,830 if SPX expires anywhere below $106 for Aug OPX.

The reason that I don’t engage in a typical credit spread is because of a low return/high risk structure. People typically make 5% of the total investment in a matter of 6 to 4 week timeframe, and yet, from a probability standpoint, 3 out of 10 positions would go out of money and, therefore, the chances of making money consistently with a credit spread is very low (one big loss could easily take out of 10 months worth of return).

Because of this reason, I won’t use this option strategy — except for one condition that I’m going to discuss in here shortly. Credit spreads become a very powerful strategy when it’s applied against a major support/resistence level.

Major support/resistence levels

When the underlying stocks are hitting against very strong support/resistence levels, the credit spreads below/above the support/resistence levels would become a very powerful strategy with a much better risk/reward compared with a regular credit spread. It would be even ideal if the breakeven on the credit spreads matches with the underlying stocks’ support/resistence levels.

I’m going through 3 examples here with Qs, GS, and XLE. All these stocks/ETFs are hitting against a major resistence level, which makes it worthwhile to set up a credit spread with more than 50% rerutn in 2 weeks.

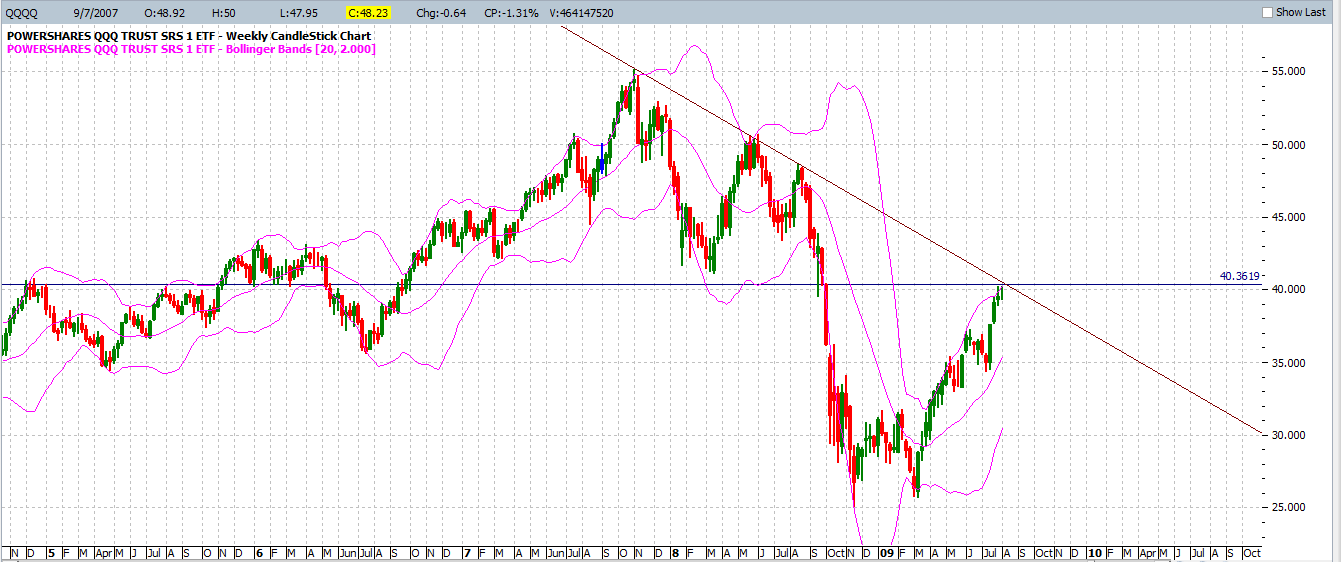

QQQQ Credit Spread

As you know, Qs did NOT participate in the rally for the past week whereas other major indices were making new highs on Friday. Qs is hitting against a major resistence level with the recent high of 40.19.

Here is Qs 40/41 credit spread. You buy Qs Aug 41 call optioons and sell Aug 40 to create Aug 40/41 credit spread. You make $380 off of a total cost of $620. This is a more than 50% return in 2 weeks. Imagine how many trades you have to make with the futures in order to make more than 50% return in 2 weeks?

Qs Credit Spread Strike Price: Short 40 Call, Long 41 Call

Stop Loss: 40.20

Risk/Reward: $380/$91 (Stop Loss)

Return on Investment: $380/$620

Probability: 62%

Hold on to your position until OPX as long as Qs stays below $40.

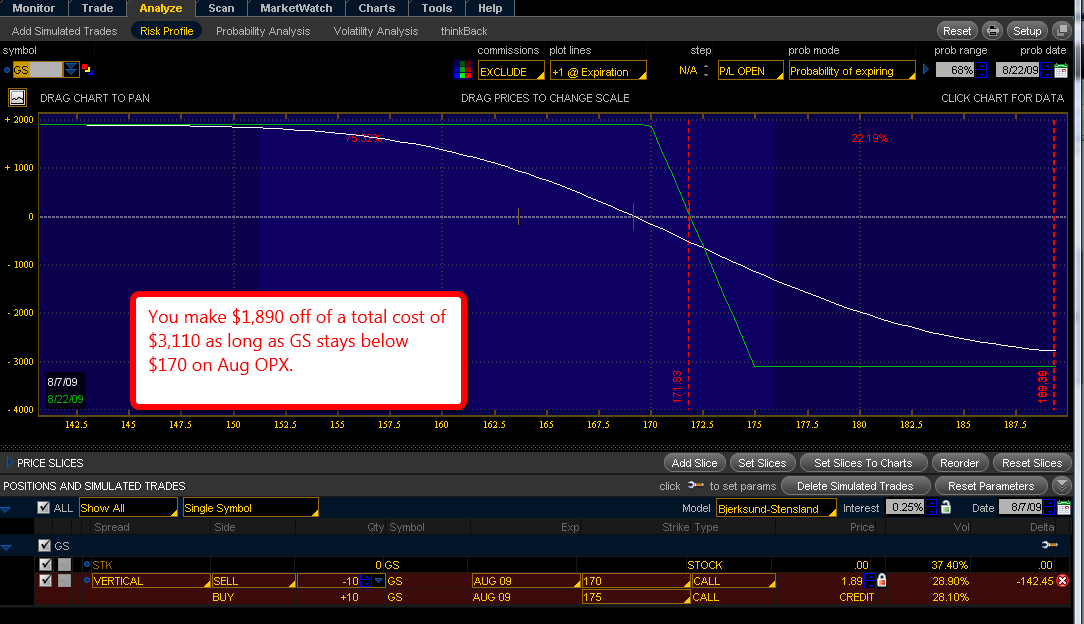

GS Credit Spread

GS was one of those stocks not rallied on Friday. GS has a strong resistence level right at $170. Please also note that GS is forming a mini H&S pattern (!) on a daily.

Aspenman pointed out that my PL graph on GS does not work. That was the error on my part and after looking at the revised PL, R/R does not work any longer so I decided to take the whole thing off.

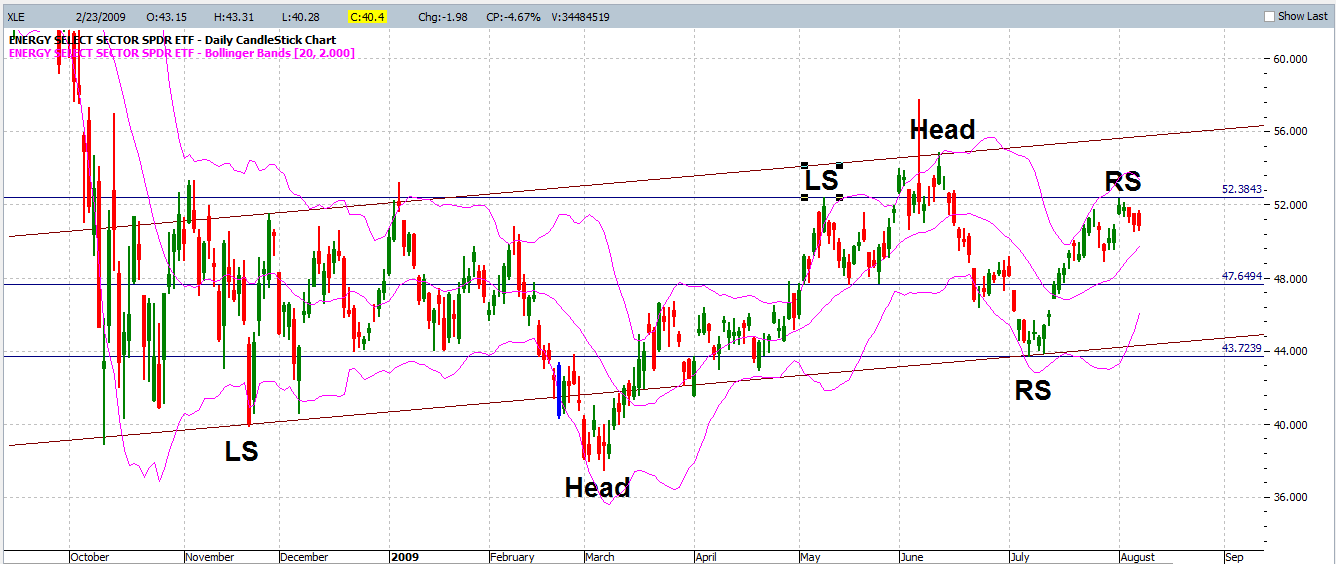

XLE Credit Spread

OK, I know many of you don’t want to hear one more word of H&S, but I see both H&S and IH&S in XLE, and it’s hitting against RS resistence level at $52.28. I don’t know which one is going to pan out at this point, but I’m taking a short position on this one.

Here is XLE Aug 52/53 credit spread. You buy XLE Aug 53 call options and sell 52 call options to create 52/53 credit spread. You can hold on to this position as long as XLE stays below $52.

XLE Credit Spread Strike Price: Short 52 Call, Long 53 Call

Stop Loss: $52.29

Risk/Reward: $320/$203 (Stop Loss)

Return on Investment: $320/$680

Probability: 69%

Hold on to your position until OPX as long as XLE stays below $52.

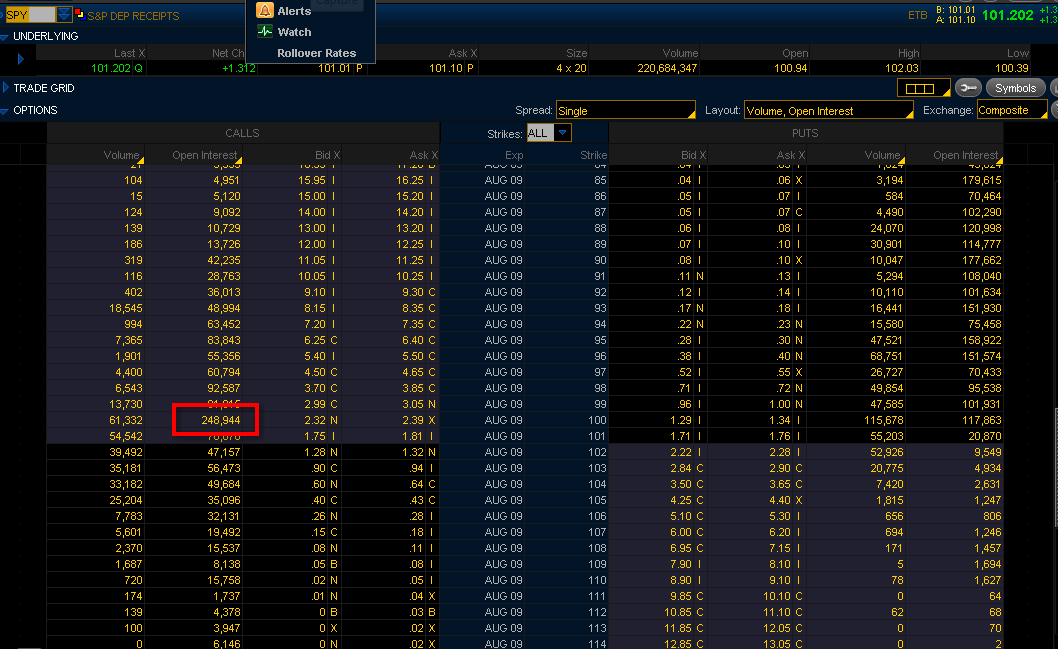

SPY Iron Condor

Lastly, here is my SPY Aug Iron Condor. My SPY OPX projection would be around 100 based on the open interests.

I’m planning to put on 96/98/103/105 Iron condor on Monday. ROI is 100% ($1,000 return on a cost of $1,000) and I’m going to close the legs if SPY closes above/below my breakeven points of 97 or 103. Otherwise, I will just keep them until OPX.

Passive Position Management

Beauty of these credit spreads is that you don’t need to manage it every minute, every hour. You can put this on together with a stop loss, and then go outside and have fun. Come back and check your position at the end of the day to see if the underlying is still below the short strike. You can easily make 50% return in a matter of 2 weeks on your investment with passive position management.

For an advanced option trader, you are more than welcome to add on the other side of the credit spreads right above the support level to make it iron condor.

Covers two directions

Another benefit of credit spreads is they cover two directions; i.e., down and sideways. Even if the stock doesn’t do anything at all until OPX, you can still make money as long as they stay below the short strike. As you may be aware for the past 3 months, the market does not go down when consolidates – it merely goes sideways until it’s ready to make another move. You won’t get jitterly with credit spreads when the underlying is not making any immeidate move. In fact, you ARE making money on positive theta, and in addition, the upside movement is limited by a resistence.

Give me your candidates!

I only went through 3 credit spread examples here, but if you have other good candidates, please let me know. We can make it as a group effort to come up with good credit spread candidates so that we are all ready to rock’n’roll on Monday!

Here are the criteria:

1. Stocks hitting against a major registence level. Not participated in the rally on Friday, and ready to roll or already rolled over.

2. Risk/Reward should be more than 1 to 3.

3. Return on investment should be more than 50%.

I will update this list at the end of this weekend so bring it on!

Once again, imagine, trying to make 50% return with the futures in 2 weeks. How many trades do we have to put on? And yet not all the trades are going to be winners.

We only have so many weeks left for the summer (at least here in Seattle). Let’s take it easy, put the credit spreads on, and enjoy the summer.

Fujisan.

Saturday 7:00 pm (PST) update:

Is a call credit spread the same as a put debit spread?

Mr. clam was asking me if these call credit spreads are the same as put debit spreads. Yes, they are technically the same, but the cost of the commissions would be different. When you are trading smaller ETFs like Qs and XLE, we are going after $300~$400 profit (per 10 contracts) and if you are a regular TOS customer paying $1.50 for a commission, you would have to pay $30 commission for 10 credit spreads, which accounts as much as 10% of the entire profit. Now, the beauty of the credit spreads is, as long as the underlying stocks stay below the short strike, you don’t need to buy them back. You can just let them expire as both longs and shorts are out of the money, so you are saving $30 commission (10% saving on the profit). On the other hand, if you are putting on a debit spread, both short and long strikes are “in the money” so you have to buyback before OPX in order to avoid the stock assignment.

Setting up a stop

Josh was asking me if the stop loss is EOD. Technically, when the market takes out the previous high with a much lighter volume and closes below the previous high’s close, this is considered to be a successful retest of the previous high and therefore, I would not recommend that you close your position simply because the previous high was being taken out.

However, for those people who cannot watch the market at the close, they might as well put the stop in to protect their capital.

Sunday 7:30 am (PST) Update: Aspenman pointed out the my GS PL graph does not work. That was the error on my part. The price was locked in somehow and did not reflect the true value. After reviewing the graph, R/R does not work anymore so I decided to take the whole thing off.

{kind=link}