Risk Management

Risk Management

Fujisan here.

In my last week’s posting, I discussed hedging technique to protect the open positions, but I quickly learned that not many of you used this technique when the market edged up to retest the recent high. I saw some comments on Wednesday asking what they should be doing with their underwater Qs option spreads. Well, unfortunately, there is no magic adjustment to turn losses into gains, and that’s why it’s very important to exit the position at the right time.

Without a proper risk management, you could quickly lose your capital, and options could be a highway to hell instead of heaven.

Risk management is always a very important concept when it comes to trading, but it is even more important to option strategies, and that’s what I am going to discuss today.

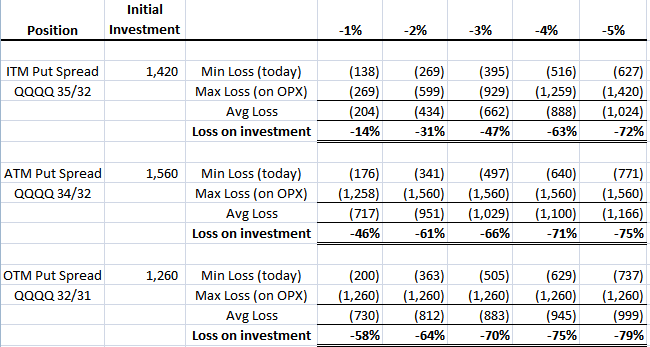

Loss on Investment

Please take a look at this schedule. This is a summary of potential losses in Qs June bear put spreads with different strike prices if Qs makes adverse price movements. As you can see, the further Qs moves away from the entry point, the more the losses expand.

This is the reason why you cannot “buy and hold” directional option spreads (there is a “buy and hold” option strategy with delta neutral position, but that’s not what we are talking about). You have to have a very tight stop (both price and time stop) and active position management in order to avoid the “exponential” loss situation as illustrated above. But here is a question. How often would my stops possibly be hit if I have a very right stop? Very often. That’s why I’d rather have “hedging” strategy than a regular “stock loss”. I will discuss this further.

Risk/Reward Calculation

OK, we now know the importance of a tight stop. Now, here is another piece of the puzzle. If you expect to be taken out of the position, as often as 50%, then you’d better have a better risk/reward ratio, right?

You bet you do!

Here is what I do.

I have a very specific entry/exit point, and I calculate the risk/reward (RR) ratio based on that. If RR ratio is below 300%, I won’t take the trade. I only take the trade if RR ratio is more than 300%.

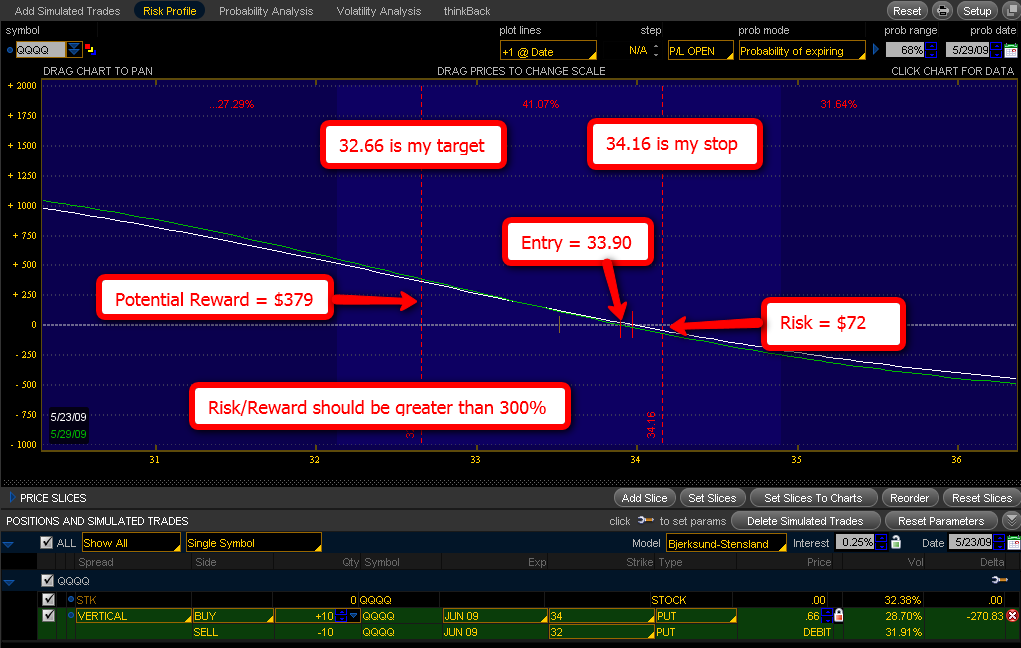

This is Qs 34/32 bear put spread P&L graph and these are my trading plans for this time around:

Entry: 34.90

Immediate Target: 32.66~32.24

Stop Loss: 34.18

Time Stop: May 29 (if the position is not in the money, close it by this date).

Risk Reward: $379 (reward)/$72 (risk) = 526%

I normally trade in a much longer term (meaning a few weeks to a month), not in days, but these days, I am trading in a much shorter time span, and this is not what I’m looking for – but what can we do? The market doesn’t care how I trade. If I like to trade the way I do, I should probably stay out of this whipsaw market and wait for a major move — there are so much works to be involved and so little money to be made. I’m sure that many of you share my sentiment. In the mean time, I should trade small.

Diversification

Now, one more thing that you can do as a part of risk management is to diversify your position. No, not that kind of diversification (yes, that one too), but diversification through different strike prices and expiration months. Don’t just marry to one position.

If you have $1,000 budget for Qs directional trade, allocate your capital into different positions. Don’t just put everything into one bucket. You can have bear put spreads with different strike prices and expiration months. Or you can have butterflies and calendars other than bear put spreads. You don’t need to trade front month options all the time. Mix up your positions so that you don’t get hurt entirely in case the trade goes against you.

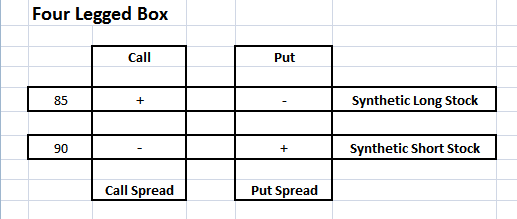

Four Legged Box

Lastly, I like to go over the basic concept of hedging. Although I discussed this topic last week, I think I should go over this again as this is a very important part of risk management.

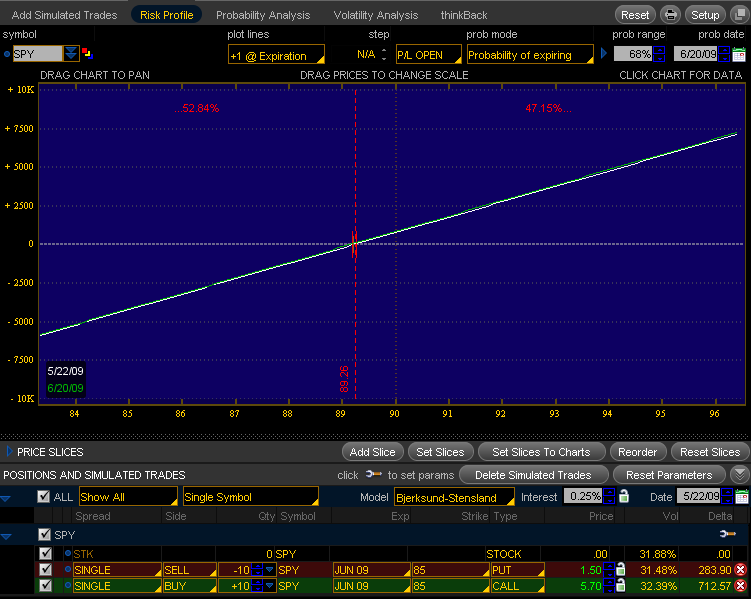

Options are very flexible financial instruments and you can recreate any type of “synthetic” stock positions. For instance, in order to create synthetic long stock position, you simply go long call options and short put options and, voila! This looks exactly like long stock position. This position is a combination of long June 85 SPY call and short 85 put options.

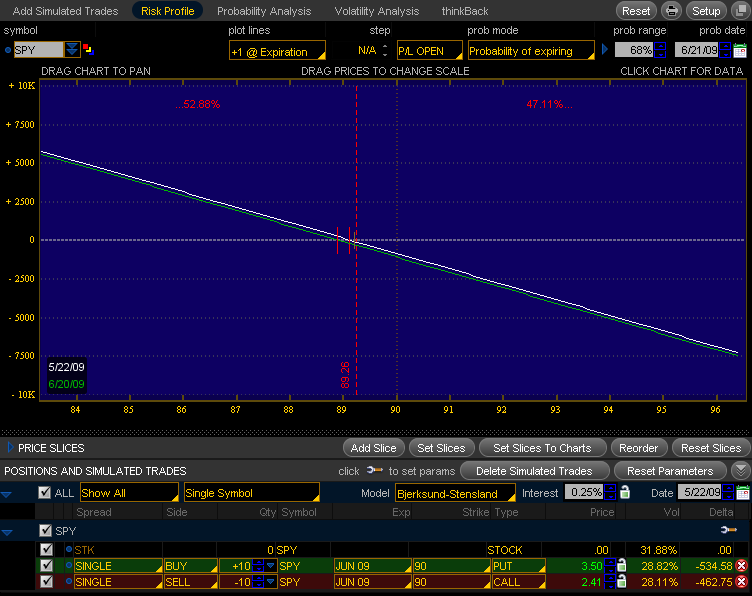

In order to create synthetic short stock position, you simply go short call options and long put options. This has the same P&L curve as short stock position. This is a combination of long June SPY 90 put and short 85 call options.

Now, if you combine long and short stock positions, what do you get? It’s a flat position, and you don’t make money in either direction. This is called “Four Legged Box”.

Now, four legged box in itself is not tradable, but you can leg out into four legs.

If you look at the four legged box matrix above, and take a vertical instead of horizontal combination, you will get a bull call spread with long June 85 call and short 90 call options.

Similarly, if you long 90 put and short 85 put options, that would create a bear put spread.

If you combine a bull call spread and a bear put spread (with the same corresponding month and strike price), that will become a “four legged box”.

Now, how can we use this concept?

Let’s say that you originally entered into June 85/90 bear put spread and you are expecting the market to take a short-term turn. You still expect the overall trend to be downside and you like to hold on to your position, but you don’t want to lose a profit already made. What can you do?

Yes, you can leg out June 85/90 bull call spread and make “four legged box” to lock in the profit. Moreover, you can add on call spreads to ride to the upside as well.

….or, you can make a “three legged box” by adding June 85 call.

Hedging is not just locking in the profits. This also gives you an opportunity to ride to the other side of the trade and make money in both sides. I made more money by being stopped out and turned into other side of the trade.

This is such an important concept especially now that we expect whipsaw galore for the coming weeks, and if you don’t want to get in and out of the positions every other day, hedging is the best way to go.

This is really not as complicated as it may sound. You just have to try it once to see how it goes. I’m almost certain that you will love it!

Have a wonderful weekend, everyone!

Fujisan

May 23 Update: Squidman brought up a very good question about naked put option adjustment, so I decided to address his question here, as many of you are trading naked options.

His original position was June Qs 33 put options, and he adjusted it with 35 call option. With this adjustment, he was basically creating a strangle which looks like this.

As you can see, breakeven point is almost outside of one standard deviation and you are running a risk of losing the entire premium in both call and put options in this adjustment. In other words, you are throwing a good money into a bad trade without no hope of recoupting the cost of the trade.

What if you adjusted Qs 33 put options with 33 call options? This is a little bit better than strangle but the results are the same. Moreover, you would have been putting more money into the trade and the cost of the investment doubled whereas the return potential didn’t.

With this adjustment, you would be creating a straddle which looks like this.

If you really like to adjust your position, you would have to recreate 4 legged box by

1. shorting 32 June put option and,

2. adding 32/33 bear call spread

to lock in a loss. This position has the same P&L effect as closing out the position, but I would say most of the people would be better off just by closing it out instead of messing around with all kinds of adjustments that you are not entirely familiar with.

Trading Rules

If you are still buying naked options, please do yourself a favor and follow these rules:

1. BUY ONLY ITM (in the money) options for the front month. DO NOT BUY ATM and OTM front month options. Please be prepared to lose the entire premium if you are trading front month ATM/OTM options.

2. BUY ONLY the back months options at least 60 days before the expiration, if you are trading ATM/OTM options. Close it out in 30 days to OPX.

Happy memorial holiday!

Fujisan

UPDATE 5:45pm EDT: Mole here. This is a great opportunity to talk about something I meant to convey a while ago. The concept Fujisan describes is actually also known as ‘morphing‘. In effect what she is doing when producing a ‘three legged dog’ is to turn her bear put spread into a something very near to a synthetic long call. Let me explain:

As she described a synthetic stock positions is accomplished by buying a call and selling a put:

|+c| = Synthetic Long Stock

|-p|

Similarly a synthetic short positions is produced by selling a call and buying a put:

|-c| = Synthetic Short Stock

|+p|

Now, I will spare you the ugly details regarding the greeks calculations but the concept you need to remember is that 100 shares of stock plus one option is considered a synthetic option:

|+c| -c = -p = Synthetic Short Put

|-p|

|-c| +c = +p = Synthetic Long Put

|+p|

|+c| +p = +c = Synthetic Long Call

|-p|

|-c| -p = -c = Synthetic Short Call

|+p|

Here I am representing the long or short stock position via their synthetic option equivalents – bear with me here. I actually came up with that visualization myself after watching Ron Ianieri’s video on the concept – he is a great instructior and knows this stuff inside out but I was seeking for a simple mental recipe to execute trades quickly.

So, if you look at those four variations above – all you have to do now is to fill in the missing leg on Fujisan’s four legged box – which is to buy one 85 call, just as she described:

|+c85| +p90 = +c = Synthetic “Long Call”

|-p85|

Now, the acute rat would point out that this is not exactly correct – for a synthetic long call all three strikes need to be the same:

|+c85| +p85 = +c = Synthetic Long Call

|-p85|

Obviously this is technically impossible as you cannot buy/sell a put at the same time – you end up neutral which only leaves you with the call – and hey that would be the idea. A real synthetic call would be produced by being long the stock and long one put. Yes yes – I know it sounds strange but the delta works out perfectly.

In any case, the red scenario is what you want and it’s close enough to a synthetic long call to accomplish your goal. What’s even cooler is that all you had to do was to buy one option instead of having to sell two and then buy one. Your positions is exactly identical and you pay a lot less in commissions.

Cheers!

{kind=link}

{kind=link}