Summer Earnings Expedition

Summer Earnings Expedition

Summer earnings season is my least favorite by far due to muted volatility across the board. However with a bit of skill, finesse, and duct tape we ought to be able to squeeze a few R out of this one by focusing solely on IV outliers. Before we get to this week’s goodies let me be crystal clear that the one and only way to play earnings is via options – period. So if you do not currently have an options trading account then I recommend you open one with either ThinkOrSwim or TastyTrade.

Also in case you have forgotten or are new here: The name of the game is to do the exact opposite of what you’ve been taught on MSNBC or other financial MSM outlets, which is to largely ignore direction and instead focus on trading implied volatility (vega) as well as time (theta).

The strategies we will employ is to trade weekly options as follows:

- Short Calendar spread (far OTM beyond one of the EM thresholds).

- Short Diagonal spread (far OTM beyond one of the EM thresholds – with front month long strike a bit further toward the money to reduce blow out risk).

- Short Strangle (far OTM on both sides of the two EM thresholds).

Most of the positions will be taken at least 3 days prior to each issue’s earnings announcement. We usually close it out right after the announcement or the next day if the announcement is scheduled after hours.

As an experiment and in order to perhaps slightly shift the odds in my favor I will also consult seasonal statistics. This is something that sort of popped into my head the day and as this constitutes a new approach I will use small position sizing in order to minimize the possible damage should this strategy turn out to be flawed.

BAC – earnings on 7/16 before the open.

7/17 series IV: 77%

7/25 series IV: 62%

Weekly EM: 1.7

Stats suggest a bullish bias.

Which means I’ll be selling an OTM calls < 25.

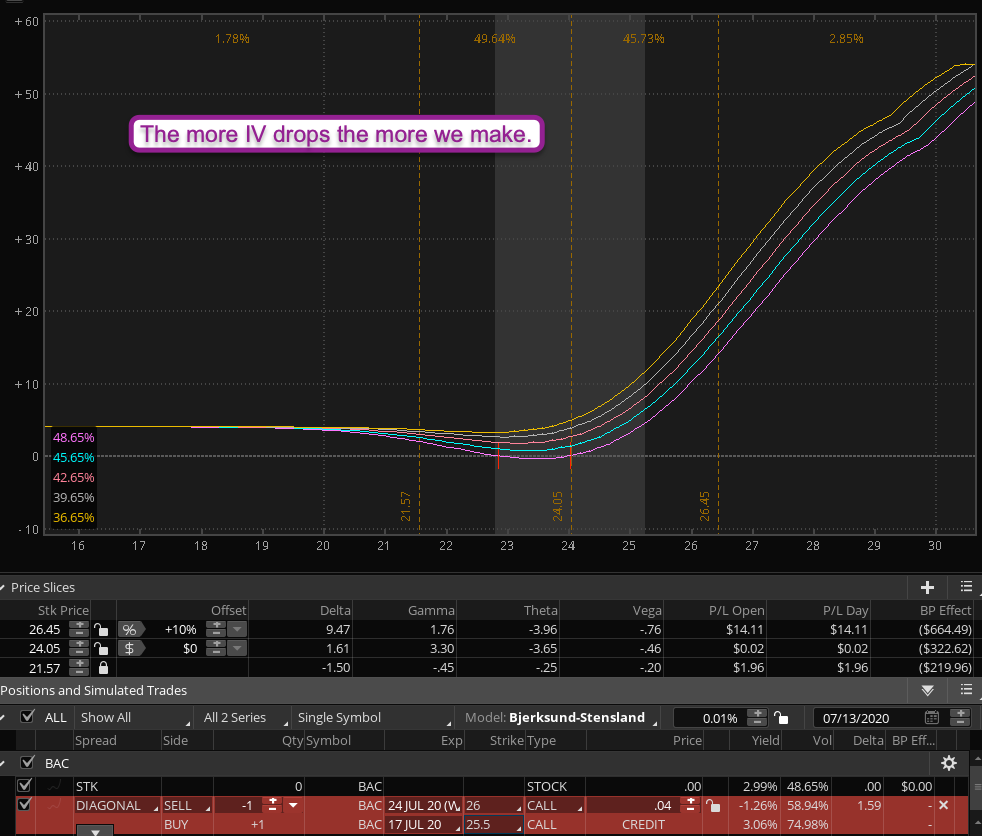

Here’s an example. As you can see this strategy greatly benefits by a drop in implied volatility which does affect the front week we are buying but also the back week we are selling.

SELL -1 DIAGONAL BAC 100 (Weeklys) 24 JUL 20/17 JUL 20 26/25.5 CALL @.04 LMT GTC

More earnings setups below the fold for my intrepid subs:

It's not too late - learn how to consistently trade without worrying about the news, the clickbait, the daily drama and misinformation. If you are interested in becoming a subscriber then don't waste time and sign up here. The Zero indicator service also offers access to all Gold posts, so you actually get double the bang for your buck.

Please login or subscribe here to see the remainder of this post.