Well Positioned But Skeptical

Well Positioned But Skeptical

Last week’s decision to hold through a trading bot driven low participation reversal higher appears to have been a good one as of right now. At least the campaign managed to survive the weekend and that’s no small feat in this volatile market environment, which incidentally is why I am choosing my words very carefully. The ides of October often bring us stormy weather as well as volatile markets. Given ongoing fears of a large scale sell-off another momo update seemed appropriate.

Volatility skew is the difference in implied volatility (IV) between out-of-the-money options, at-the-money options and in-the-money options. Volatility skew, which is affected by sentiment and the supply and demand relationship, provides information on whether fund managers prefer to write calls or puts. It is also known as a “vertical skew.”

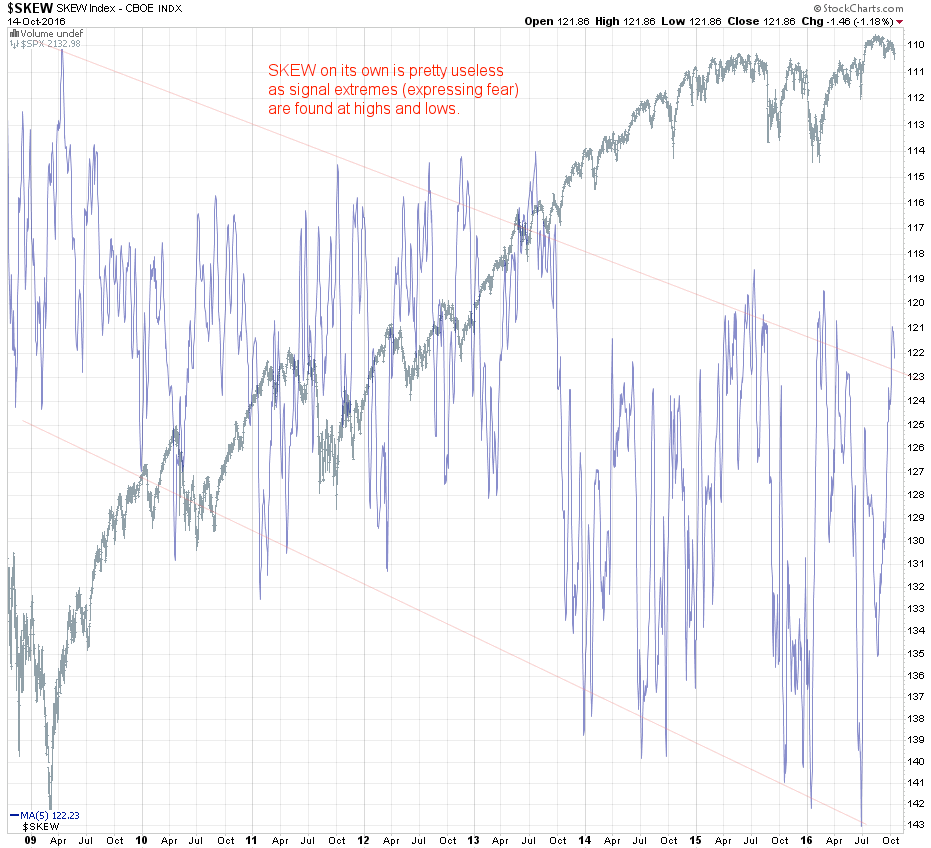

The CBOE SKEW Index (“SKEW”) is an index derived from the price of S&P 500 tail risk. Similar to VIX, the price of S&P 500 tail risk is calculated from the prices of S&P 500 out-of-the-money options. SKEW typically ranges from 100 to 150. A SKEW value of 100 means that the perceived distribution of S&P 500 log-returns is normal, and the probability of outlier returns is therefore negligible. As SKEW rises above 100, the left tail of the S&P 500 distribution acquires more weight, and the probabilities of outlier returns become more significant. One can estimate these probabilities from the value of SKEW. Since an increase in perceived tail risk increases the relative demand for low strike puts, increases in SKEW also correspond to an overall steepening of the curve of implied volatilities, familiar to option traders as the “skew”.

What I have done above is to invert the SKEW index and superimpose it on the SPX in order to determine if it has any predictive quality. And in my not so humble opinion it has very little if any for the main reason that the determination of IV (and thus the pricing of options) do reflect an anticipation of future risk. This may be due to seasonality, prior events, anticipated future events, etc. Which is why we see signal extremes (i.e. drops lower or spikes higher) during major highs and lows on the SPX. The magnitude of the signal extremes also do not correlate well with the accompanying changes on the SPX. So once again risk perception is not only relative and subjective, it’s also both lagging and anticipatory. Why else would be see a signal near the 120 mark both in July of 2015 (near the highs) and in March of 2016 (near the lows)?

Which is why I usually correlate the CBOE SKEW index with another measure of risk. In the case above I’m using the VIX which pretty any trader with a pulse is familiar with (very few can explain what it’s comprised of but that’s for another day – hint: look up VIN and VIF). Now although VIX in itself is certainly another discretionary measure of risk, the two combined do seem to be more predictive. Of particular interest to me has been a repeating pattern of ratio compression followed by a pre-tremor, followed by a deluge (of selling).

Circling back to the current short campaign. This is one of the main reasons why I am still very skeptical about the downside potential here. We are certainly compressing the range but we have a) more room for the diagonal to rise and b) we have not even see a pre-tremor yet. Or maybe we are about to paint one. Only time will tell – in the interim call me well positioned but extremely skeptical.

But we’re just getting warmed up here, Spock’s blue light emitting prop has uncovered some very unusual signal divergences:

It's not too late - learn how to consistently trade without worrying about the news, the clickbait, the daily drama and misinformation. If you are interested in becoming a subscriber then don't waste time and sign up here. The Zero indicator service also offers access to all Gold posts, so you actually get double the bang for your buck.

Please login or subscribe here to see the remainder of this post.