A Trader’s Guide to Contractions

A Trader’s Guide to Contractions

I may be a little early on this, but this is not a timing call. This is food for thought, better digested while the sky still remains high.

Michael Davey (CD) here…

Two important truths about the market which tend to be ignored, especially by the investing public, are 1): Stock prices reflect a market’s premium-to-growth for a given company; and 2): When a glass is truly full, there remains only fractional potential for the volume of matter to rise; while the potential for volume to decrease is more significant. This does not speak to timing, which is important in trading, but more to the points that when everyone is on the ship, at some point there is no one left to come aboard.

The first point is crucial, but the general public does not think of stocks in this way. When they perceive a company as bad, they can’t see the logic in the stock of that company rising. At the same time, if they recognize a superior, excellent company with an innovative and diverse product line, they expect the stock should be good as well; especially if they know the stock to have traded at rich price-levels and have become accustomed to that level of price for that stock.

But this is very dangerous, since stock prices do not represent the quality of a company, but instead a market’s premium to that company’s growth.

If I show you a company (XYZ) which has been growing steadily at 10% per year and XYZ has a PE of 20 (price-to-earnings ratio), the premium-to-growth is rather rich. Why? Because the company is selling for twice their rate of growth. Ironically though, the stock’s low PE suggests a more modest valuation. A better measure then for quickly measuring valuation is the stock’s PEG. PEG = PE/Growth; 2.00 in the above example.

Conversely, if I show you a younger company (ABC) which is growing rapidly at 100% a year, but sports a PE of 50, the premium-to-growth here is significantly lower (a PEG of 0.5 in this case). Even though we have a significantly higher PE, the valuation is less richly valued.

Stock prices are a measure of supply vs. demand, so in the above example the market is (currently) pricing XYZ with a higher premium-to-growth than ABC. Even though XYZ is slow-growing compared to ABC, ABC is priced less than XYZ (regardless of what price-per-share each company is trading at, since that could be almost any number; dependent only upon an arbitrary number of shares outstanding. Thus, ABC might trade at $100/shr and still be cheaper than XYZ which might trade at $10.

This might be dummed-down for most of you, but might be important/informative to others. Keep reading Einstein – I might finally get around to saying something!

The peanut gallery might point to ABC’s PE of 50 (like Barron’s) and write a weekend (zzzz)report on how over-valued that stock is, blah blah, etc. etc. Meanwhile, the same rag might feature the mature ABC stock on the cover as being cheap (especially if the stock is in free-fall!); since it is an established brand and has a reasonable PE of only 20.

Here is where it gets interesting. I could show you the greatest retail company of the next 10 years (possibly the name pictured above) and if the PEG is very richly priced, the company could grow every bit as currently anticipated and more, and yet the stock will quite possibly decline at the same time.

I’m exaggerating, obviously, since that can’t be true.

Well, actually no.

Let’s examine a couple of great retail stocks of the past – Starbucks and Walmart (there are more, but you and I are short on time). We can all agree these are two titans in the history of retail. Walmart grew to such enormous heights that today it accounts for something like 10% of total retail sales in the US, while Starbucks, at it’s peak, was practically within spitting distance of every step you ever took (certainly in this country).

Fine. But did you know that while Walmart was growing into the monster it is today, there were periods of solid, continued growth where the company traded lower for years at a time (the 1990’s being the best example). This is known as a PE-contraction (essentially, even though a company continues to grow, perhaps even better than expected, the premium-to-growth can decline at a more rapid rate).

That premium can decline for any number of reasons (interest rates, market conditions, trends, money flows, animal spirits, still-further anticipated growth, etc.). The point is that a good company on its own does not guarantee a good stock (if you weren’t bored by the first half of this piece then re-read that sentence).

Starbucks this year is expected to earn roughly twice the amount the company profited 5 years ago, but the stock is cheaper by almost 50%. Even though the company generates twice as much profit, investors have lost half their investment; thanks to a PE-contraction.

Now for the second point – that a glass full has more to empty than to fill further. This is not to say that something overvalued cannot go higher, or that an undervalued company cannot see its stock trade lower (no no no). Rather, that when the market participants (institutional and private investors) have all taken their position in a stock, (or have all sold their position, on the other extreme), then there remains little space for that stock to rise (or fall) further. If there are 1,500 institutions capable of taking a position in a given company and 1,400 of them already hold a stake, the supply of institutions is already saturated and the ability of the remaining 6 or 7% to take the price higher is obviously limited. We can argue for some length what these levels are, for both institutions and retail investors, but no matter – at some point there are no more outsiders to come in and drive up the price.

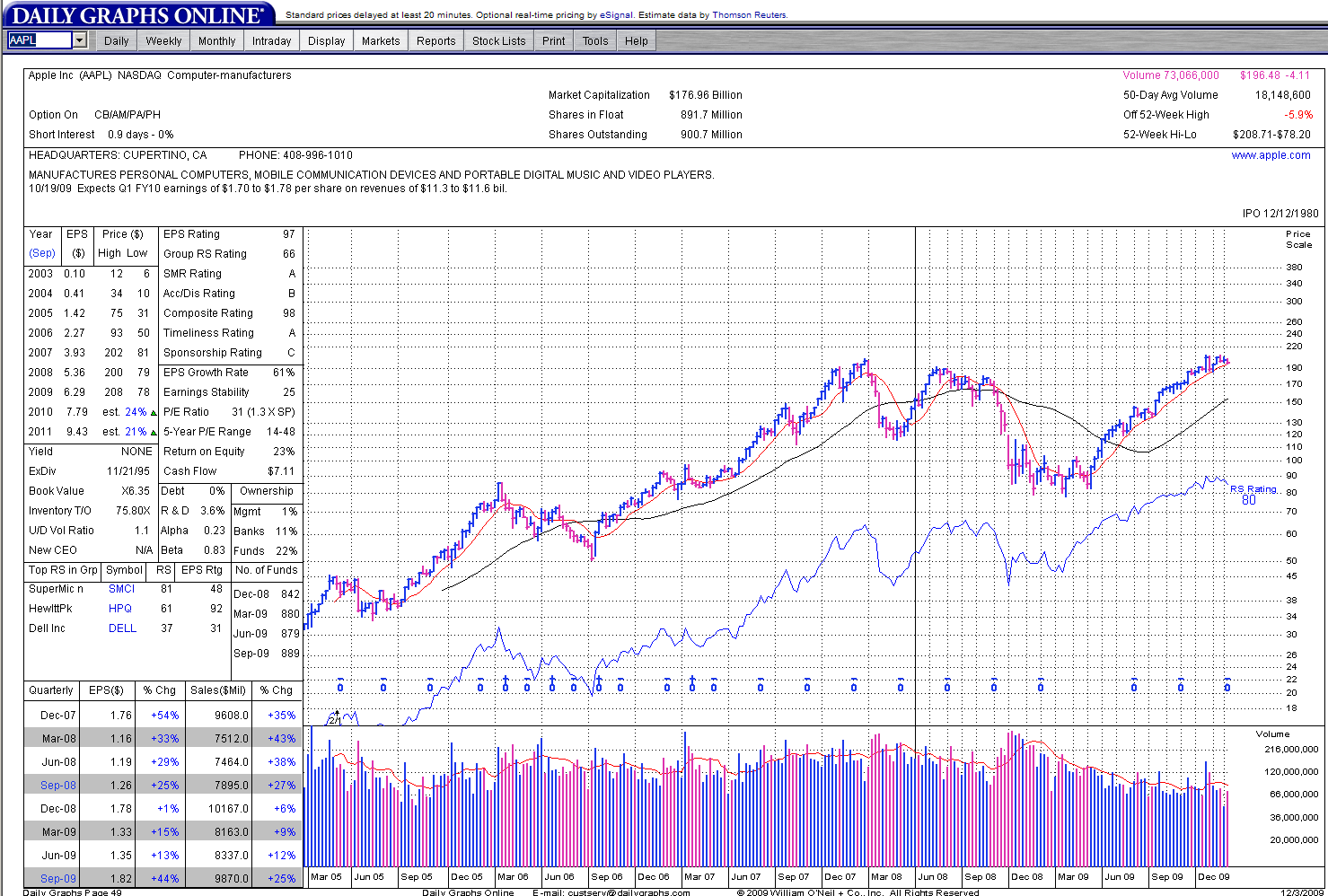

Even if it’s a company as amazing as…Apple Computer.

There goes the majority of my reading public right there forever (and there goes my widow and orphan friends to boot). Am I stupid enough to attack the stock of the greatest company in the world and suggest you fools SELL?

Nah.

I wont do that to you – to us! I know you have a time horizon of X; and you have a pain threshold of Y; and your tax-gain consequence is Z; and the percentage of AAPL relative to the rest of your portfolio is XX; and that portfolio relative to your worth is YY; and so on forever.

I know none of that, obviously. Please understand then that I am suggesting absolutely zero as far as what you should do with your investment of Apple Computer.

I just want to make the point, since it takes too long (and too many drinks) to do so at parties – that you may own the greatest company since bread was first sliced and that company may grow ever to the sky, and you still may lose money on the stock.

Besides the fact that AAPL is the premier institutional growth stock and the glass of managers in the stock by this point is reaching full (saturated, crowded investment), history shows us that a PE-contraction can overwhelm even the greatest companies, and even while they generate greater and greater profit.

How about AAPL‘s PEG? There is clear precedent for concern. APPL’s PEG based on current earnings is quite high at 1.79; while the PEG for estimated 2010 earnings is still high, at 1.29. Apple’s current PE of 31 is quite a bit higher than for other box and handset manufactures and deservedly so – this speaks to their innovation and their ability to round up consumers, selling to them on a variety of connected products and spaces. And while I’m not suggesting that Apple will disappoint in the future, my argument is that it doesn’t need to disappoint in order to see a multi-year decline (even if the broard market rises during the same period!).

The simple point here is that Apple’s premium-to-growth (the premium which has been elevated by a multitude of players getting into the now very-full glass) will be what drives the price; regardless of whether or not Apple transcends into the dominant retail force it is suggesting.

If Apple fails to grow that dominance, well even my widow and orphan friends know then it’ll be a disaster for share holders. What I don’t think they’re conscious of though, is that they’re in for pressure, perhaps likely, even if all those Apple dreams all worm true.

Previously in this series:

A Trader’s Guide to Sipping Kool Aid

Losing Like a Winner: A Trader’s Guide

A Trader’s Guide to Secondary Offerings (Part 2)

A Trader’s Guide to Secondary Offerings (Part 1)

A Trader’s Guide (Introduction)

A Trader’s Guide to Chasing Ambulances

A Trader’s Guide to Exhaustion