Let’s Talk About Gamma Risk

Let’s Talk About Gamma Risk

In a featured comment yesterday I mentioned gamma risk in SPX and SPY options as one of the reasons explaining recent hedging activity in the VIX and ES futures. It’s a complex topic that we’ll have to peel one slice at a time. Let’s begin by considering that options in essence are multi-dimensional financial derivatives in that they exhibit sensitivity to not only price, but also time and volatility (yes interest rates as well but that’s not an issue in our current market environment).

I’m sure most of you guys are familiar with delta, gamma, theta, and vega – which we call the option greeks. I actually posted an introduction to all of them, so if you haven’t read it then I strongly recommend you point your browser here.

Delta is rather easily explained: It’s the rate of change in an option for every dollar move in the underlying. For example, if an option has a delta of 0.65, this means that if the underlying stock increases by $1, then that option will rise by $0.65 per share, all else being equal.

I often compare delta with the velocity of an option ranging from 0.0 to 1.0, whereas gamma represents its acceleration. Another way of putting it is that gamma is the delta of delta, but that’s more academic.

So why should we care about gamma? If you trade options in general you absolutely should care, but if you’re selling options, and thus are effectively delta and gamma negative, it is crucial to realize that gamma risk has the ability to wipe out your account in two seconds flat.

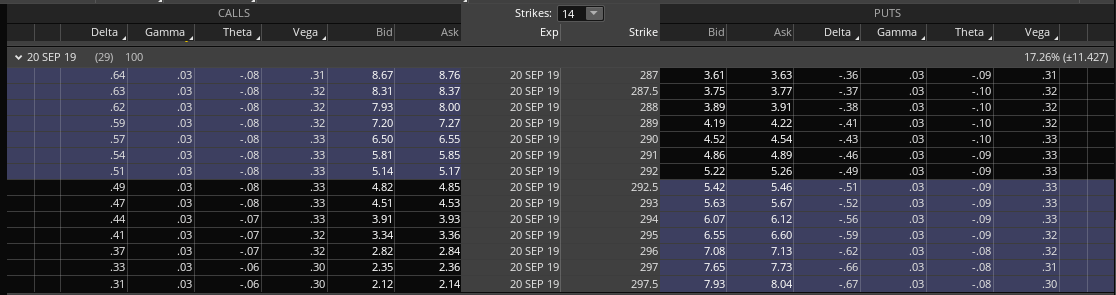

In order to understand why and how this happens let’s take a look at the September 20th option chain in the Spiders. I have selected the greeks and pay attention in particular to the gamma columns on both the call and put side.

A value of 0.03 means that delta will decrease or increase by 0.03 for every dollar move in the underlying. So if you look at the 292 call strike then you’ll see a delta of 0.51 and a gamma of 0.3. The 290 strike (one Dollar further ITM) has delta of 0.51 + 0.03 = 0.54.

So okay, gamma changes delta – makes sense. But what is the big deal?

It's not too late - learn how to consistently trade without worrying about the news, the clickbait, the daily drama and misinformation. If you are interested in becoming a subscriber then don't waste time and sign up here. The Zero indicator service also offers access to all Gold posts, so you actually get double the bang for your buck.

Please login or subscribe here to see the remainder of this post.