Option Basics – The Greeks

Option Basics – The Greeks

It’s time for the second installment in our option basics tutorial series. Today we are going to cover the option greeks – which is commonly considered a dry topic. Well that was until now – this is Evil Speculator and vee have veeyz to make you understand! So grab a short sword and a bottle of body oil because you’re going to need it down in the dusty arena when I release the four snarling beasts of the derivates (the fifth one is sleeping until further notice). I will try to make basic training as painless as possible as it is crucial that you all understand how the greeks affect the premium of an option throughout its tumultuous existence.

To set the stage let’s recall some lessons from our first tutorial:

- Options are a wasting asset. You buy one today and unless price moves heavily in your favor it will continue to lose extrinsic value every single day all the way into expiration. Given an ATM or OTM option extrinsic (i.e. time) value represents the entire premium.

- The premium of an option has two components:

- Intrinsic Value

- Time (or Extrinsic) Value

- Intrinsic value is only accumulated once price moves above the strike price of a call option or below the strike price of a put option.

- An option’s time value is equal to its premium (the cost of the option) minus its intrinsic value (the difference between the strike price and the price of the underlying).

- Time value decreases over time, eventually decaying to zero at expiration, a phenomenon known as time decay.

- Time decay is not linear – it is exponential. As a rule of thumb an option roughly loses 1/3 of its time value during the first half of its life, and the remaining 2/3 of its time value during the second half.

- Option premiums (i.e. the cost of an option) change based on:

- Changes in the price of the underlying.

- Time remaining until Expiration.

- Increase or decreases in implied volatility (IV).

- Interest rates (not a big issue in the QE era).

We covered all of the above except the third one – implied volatility, but we’ll get there soon enough. What’s important to remember for now is the trifecta of an option’s value: Price, time, and volatility. And when it comes to volatility we are only interested in implied volatility, which is not to be confused with price or realized volatility. We have covered the difference on several occasions here in the recent past and if you missed those then please point your browser here.

The option greeks you will mostly be dealing with are: Delta, gamma, theta, and vega. So if you never actually went to college and during the admission ceremony to your favorite secret society the high priest asks you what your fraternity/sorority was then just use a combination of any of those four and you should be able to avoid the black pit of pain.

Yes, I know – there’s rho but it’s only related to interest rates and we don’t really have to worry about those much since 2008, do we? Alright, let’s dive right in:

Delta

The price sensitivity of an option to changes in price is expressed by delta. Right from the get-go we need to understand that nothing in the options world changes on a linear basis. Delta is no exception there and it fluctuates constantly as it is also influenced slightly by another option greek – vega, which expressed volatility. Delta gives us a measure of the probability that an option will expire ITM. So an option with a 0.1 delta can be thought of having a 10% chance of expiring ITM – and an option with 0.9% delta is interpreted as having a 90% chance of expiring in the money – simple.

Still don’t get it? Alright, let’s use a popular analogy:

Delta = Speed

A car’s speed tells us how far a car will travel after during the period of one hour. If the car is going 60mph, it will have traveled 60 miles. Now a car’s speed is similar to an option’s delta – just replace the time component (i.e. hour) with price. An option’s delta tells us how far the option’s value will go after a one handle move in the underlying. If an option’s delta value is 0.50 and the underlying increases in price by $1.00, the option value will increase by $0.50. So a good way to think about delta is value per dollar (instead of miles per hour for a car).

But what if we ran out of gasoline and there is no price movement? If the underlying price does not move as time continues to pass (remember delta describes value per dollar – not value per hour), then option’s chances of expiring ITM starts to diminish rapidly. Which means that at expiration, all OTM deltas fall to zero. So between now and the expiration date, the delta of an option diminishes simply because time continues to pass relentlessly.

ATM options for example have a delta of roughly .50. This makes complete sense as statistically they have a 50 percent chance of going up or down. Deep ITM options have very high deltas – as high as 1.00, which effectively means that they will trade on par with the underlying instrument. Some traders use these as stock substitutes but clearly it’s not the same as holding the underlying.

Inversely deep OTM options have very low deltas and therefore change very little along with the underlying. When you consider cost like commissions and the often wide spread, low delta options are not expected to make much or any profit even despite large moves in the underlying. And that is an important consideration because comparing the deltas along the option chain is a great way of measuring the potential returns on a trade.

Option sellers (a.k.a option writers) for example regularly use option delta in order to estimate the probability that they will be assigned. Writers of covered calls do not want to be assigned and therefore use delta to assess that probability in relation with the potential return from selling an option.

Delta Range

The delta of an option ranges in value from 0 to 1 for calls (0 to -1 for puts) as it reflects the increase or decrease in the price of the option in response to a 1 point movement of the underlying asset. Far OTM options have delta values close to 0 while deep ITM options have deltas that are close to 1 (or -1 for puts as they gain inverse to price movement of the underlying).

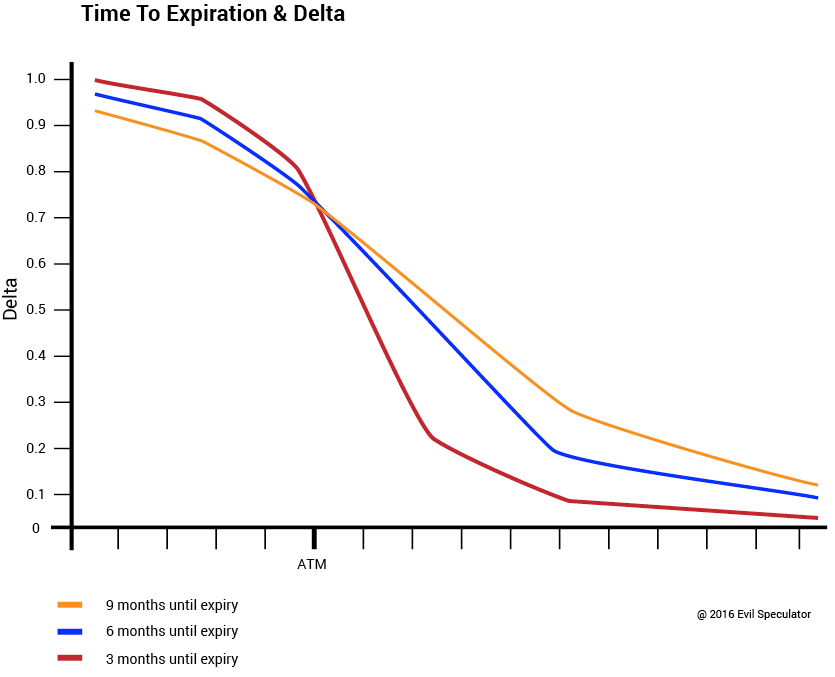

Passage Of Time And Delta

As the time remaining until expiration diminishes, the time value of the option evaporates and therefore the delta of ITM options increases while the delta of OTM options decreases. You may be wondering why the delta (i.e. sensitivity to changes in price) of ITM options expiring sooner is higher than that of the same strikes expiring several more months out.

The simple reason for that is because ITM options have more intrinsic value than time value – deep ITM options have almost no time value at all, they are all about intrinsic value. So the ITM option that is closer to expiration (red line) will have a higher premium and thus be more sensitive to price movements in the underlying.

As price rises, and the option goes deeper ITM, delta typically approaches 1.00 because of the increased likelihood the option will be ITM at expiration. As expiration approaches ITM option deltas are also more likely to be moving slowly toward 1.00 because at expiration an option either has a delta of either 0 or 1.00 with no time premium remaining.

Here’s an example: If the current price of the underlying is $50 and you are long a call with a strike price at $48 expiring in July then obviously it should track the underlying more closely than a call with the same strike price but expiring in December. The former has less time value, which in this case is considered a benefit as its odds for expiration ITM are high.

When it comes to the greeks I suggest that you worry less about the things like Black-Scholes pricing models and more about applying plain old common sense. Because it is the latter that drives the former when it comes to the proper pricing of options. That said – sometimes it can get confusing and when in doubt then come back and consult this guide

You probably noticed that the only crossover of the three expiries occurs at the ATM point – as you recall the delta of an option with a strike price ATM is exactly 0.5. Moving higher into the money starts to produce intrinsic value which is a constant (i.e. market price – strike price) and does not change over time.

Delta Gets Crushed By Time

Here’s a memory crutch for you, or should I call it memory crush: Imagine time decay as the big bully who just jumped onto the opposing end of your balance swing back when you were pondering plans for dominating the local candy distribution racket. Your end represents ITM option delta and the bully’s end represents OTM delta being crushed – ATM options are at fulcrum of the balance swing. As time progresses your end (ITM) lifts higher and the other end is being flatted – only the delta at the fulcrum remains unaffected by time.

Gamma

Gamma is delta’s little brother as they are linked intrinsically. Whereas delta measures the speed of an option (increase in value per handle or dollar), gamma can be thought of as its rate of change or acceleration. It expresses the sensitivity of delta to changes in price of the underlying asset. The more gamma the more sensitivity. Alright once again I can literally see your eyes glaze over already, so let’s go back to our car analogy:

Gamma = Acceleration

When driving a car we don’t always go at the very same speed – it constantly varies based on road conditions and traffic, and sometimes we need to take a break. When we accelerate the car, the speed at which we are traveling increases and when we step on the brakes it reduces the speed. Imagine you are driving 60mph and you put your foot on the gas and increase the speed to 65mph. The speed of the car has now increased by 5mph from 60mph to 65mph.

The acceleration of the car’s speed, that increase of 5mph, is similar to gamma changing an option’s delta value. Acceleration for a car tells us how much the speed will change (5 mph) and gamma for an option tells us how much an option’s delta value will change. That acceleration of 5mph is the moving car’s gamma – the increase in speed. Just like a car, an option never travels at the same delta during a particular trip. It accelerates and decelerates on a variety of factors. That rate of change (ROC) in delta in an option is expressed by gamma.

A car that has a lot of horse power will be very sensitive to movement. If you step on the pedal of a Ferrari or Tesla, the car will increase in speed rather quickly. So another way of thinking of gamma is horse power. An option with a high gamma value will also be very sensitive to movement. If the underlying changes, the option’s delta will change significantly.

As gamma expresses the ROC of an option’s price, it is most closely watched by participants who sell options as gamma tells us a lot about the risk potential if the underlying moves against our position. By the way, just as delta, gamma is also influenced by implied volatility (IV). More on that further below.

Theta

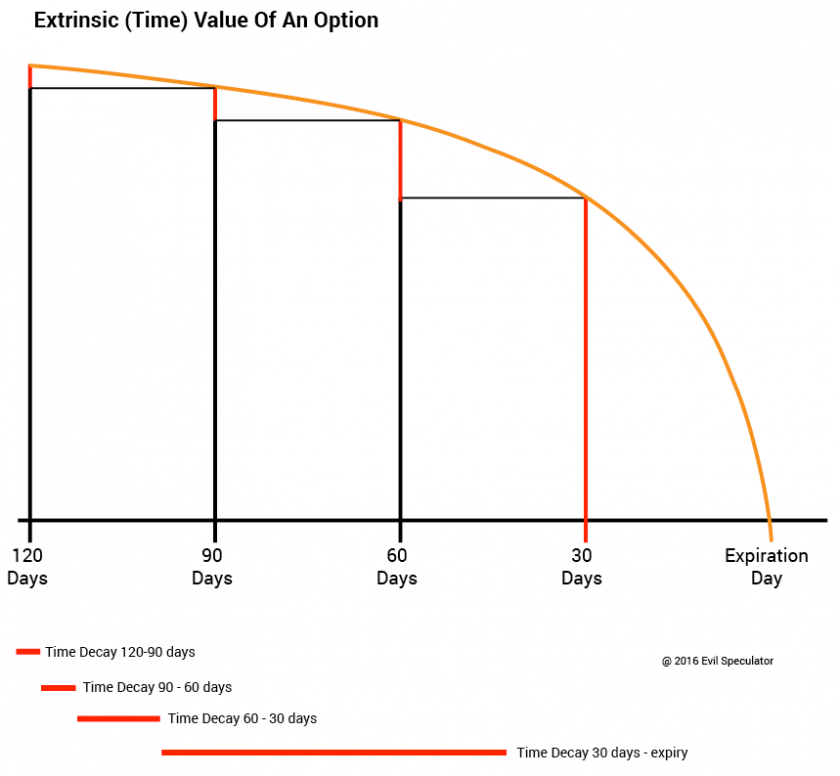

Option sellers love their theta and by now you probably can guess why. Theta is a direct measure of an option’s sensitivity to time decay. As always a picture speaks a thousand words:

As a direct measure of time decay theta is giving us the value of decay per day. This amount of value lost (in Dollars usually) starts as the proverbial trickle but slowly grows over time, until it is falling more and more rapidly the closer it gets to expiration day. As you can see from the graph shown above, the greatest loss in time decay is observed in the last month of an options life. I have copied the red lines depicting each quarterly time decay of an option to the bottom of the graph in order to better visualize the increasing loss of theta. You should burn this image into your mind so that next time someone mentions the words theta burn you know exactly what he’s on about.

Option sellers use theta to their advantage, collecting a little bit of time decay every day. Whereas option buyers hope to bank mighty coin by landing 10-bagger winners in a matter of days, the sellers are happy with collecting a few measly pennies every day but over extended periods of time. The same happens to be true for credit spreads, which are selling strategies we will cover in the future. You may have also have heard or read about calendar spreads (a.k.a. horizontal spreads), which involve buying longer-dated options and selling nearer-dated options in expectation that the nearer dated ones will lose theta faster as the longer dated ones. Again, we’ll cover all that fancy stuff in future installments of this series.

Vega

And of course I had to keep the best one for last. The vega of an option expresses the change in the price of the option for every 1% change in underlying volatility. It is important to understand that a rise in IV produces a rise in option premiums across both sides of the option chain. It doesn’t matter if you’re long a call or if you’re long a put – when IV climbs your premiums are going to get more expensive, and if IV falls then the premiums of all options fall along with it.

Many novice call buyers have learned that lesson the hard way after foolishly loading up on naked calls after a big move to the downside. As prices often snap back temporarily inflated IV will drop fast and produce a phenomenon referred to as ‘vega crush’. Although you may have picked the right direction (i.e. getting positioned long calls ahead of an appreciation in price) your may have purchased overpriced premiums which, due to a massive loss in vega, will not appreciate in value along with the underlying as expected, or perhaps even lose value.

Effects Of Time On Vega

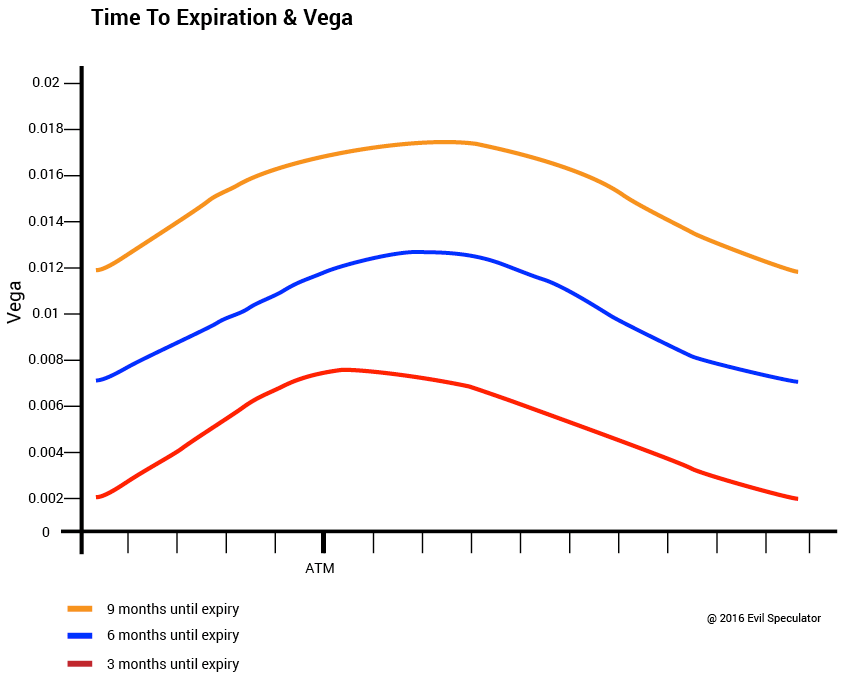

In general the rule is that the more time remaining to option expiration, the higher the vega. This makes sense as extrinsic value makes up a larger portion of the premium for longer term options and it is the time (or extrinsic) value that is sensitive to changes in volatility. Obviously the more time remains the more risk that an even more adverse price move can happen.

To demonstrate this I have produced a graph depicting the effects of vega on options at various strikes expiring in 3 months, 6 months and at 9 months. I’ve shifted current trading price (i.e. ATM) a bit to the left to demonstrate how vega peaks around it at three months until expiry (red line). How I wish I could do that in real life!

For options with expiries six months as well as nine months out that peak is shifts a bit toward the OTM call range. Vega distribution across the vertical chain is more rounded in nine month options (orange line) than in six months options (blue line) where it rises to a peak and then kind of drifts off.

And that’s it – all there is to know about vega.

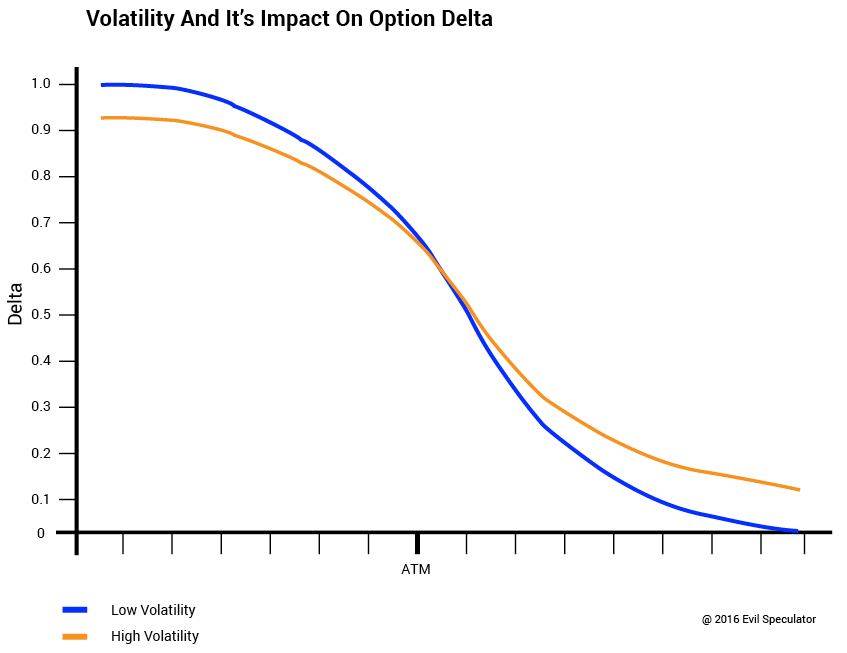

Yes of course I was kidding there, we’ve barely scratched the surface. Volatility also happens to affect option delta, because as volatility rises (orange line), the time value of the option goes up as time combined with volatility becomes more risky. I hope this makes sense. Because this is what causes the delta of OTM options to increase and the delta of ITM options to decrease. Just imagine the wings of the delta flyer I posted above and how they interact with air. As the airflow moves around the wing it increasingly produces upward pressure in the front (i.e. the OTM strikes in the option chain) and downward pressure in the back of the wing (i.e. the ITM strikes in the option chain). The neutral point is near the center of the delta’s wing which is the ATM spot.

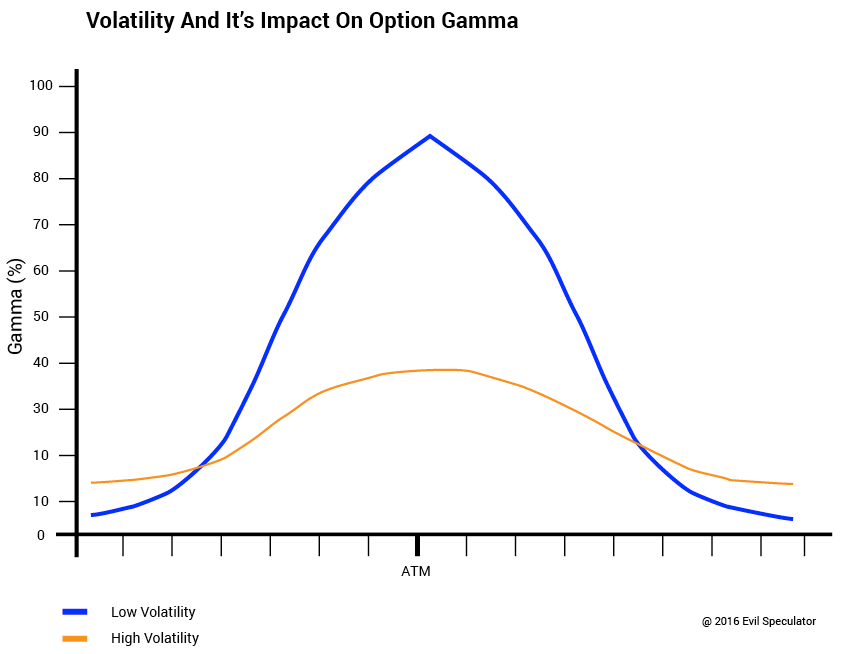

Remember that gamma expresses the sensitivity of delta to changes in price of the underlying asset – we can think of it as an option’s acceleration. When volatility is low (the blue line) the gamma of ATM options is high while the gamma for deep ITM or OTM options approaches zero. This phenomenon arises because when volatility is low the extrinsic (or time) value of such options are low. However it goes up dramatically as the price of the underlying approaches the strike price. Again this makes sense because in sideways tape the odds that either sides of the extremes are going to be touched before expiration are pretty low.

When volatility is high, gamma tends to be stable across all strike prices. This is due to the fact that when volatility is high, the extrinsic (or time) value of deeply ITM as well as OTM options is already quite substantial (remember – vega inflates time value). Thus, the increase in time value of these options as they go nearer the money will be less dramatic and hence the low and stable gamma. I know this may sound somehow backward but think about it this way: In highly volatile tape the ROC or acceleration potential (or gamma) of an option is considered to be much lower. And why is that? Because you are already flying along at 140mph – that’s why. Get it now? 😉

The graph above illustrates the relationship between an option’s gamma and the volatility of the underlying. You can see that there’s a significant difference with high volatility (blue line) producing a more platykurtic distribution curve and low volatility (orange line) producing a strongly leptokurtic curve.

If those terms just triggered a short circuit in your brain then here’s another simple memory crutch for you: Imagine gamma to be the nose of the delta plane I mentioned above. As it volatility (i.e. air flow/speed) increases it starts pushing against the nose of the plane, thus flattening it. Yes of course all delta planes are made of industrial high tensile wax, you didn’t know that?

So now you can perhaps appreciate why I mentioned above that gamma is most closely watched by option sellers. If you’re selling options near or ATM for example then this is where the risk potential is concentrated in low volatility. However in high volatility gamma is more evenly distributed and you will be most affected by a drop in volatility the closer your sold option is to the strike price. Which is why option sellers are effectively short gamma.

To wrap up volatility let’s see how it affects the option’s theta although we already mentioned this in the sections above. In the graph above you can see that options traded during high volatility periods have higher theta than options traded during low volatility periods. This is because the time value on these options are higher (vega pushes time value) and as such they have more to lose per day. As a rule of thumb: Options are historically cheap during low IV and expensive during high IV. Most likely that is one of the first things you ever learned about options.

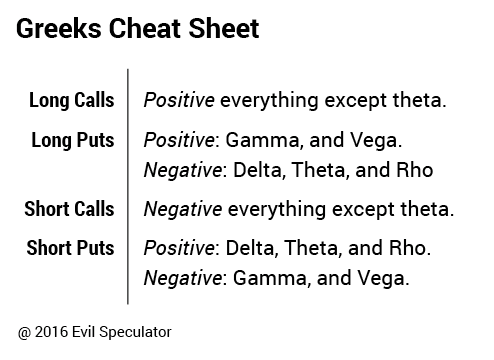

Greek Polarity

As if you haven’t suffered enough – I have prepared a handy cheat sheet I want to share with you before I send you on your way to option trading glory. At this point you probably understand that being long both calls or puts puts you into the negative (i.e. short) theta department. Being long calls or puts also makes makes you positive (i.e. long) vega. But mix in some of the other greeks and things can get confusing rather quickly. So I put together a little memory crutch for you guys and if you can remember that one you’ll be able to reside the proper greek polarity without any problem.

- First up let’s just forget about rho which is rarely considered there days (yes, purists will disagree).

- Our baseline for our memory crutch is the long call, which is positive everything, except theta. That makes a lot of sense as we talked about depletion of theta and if you’re long anything on the option side you are on the hook for theta burn.

- Inversely the short call is negative everything except theta. Also makes a lot of sense.

- Now for the long put all you need to do is to change delta from positive to negative. Repeat the words gamma/vega about 20 times and you’ll remember that long puts are only positive gamma and vega. Another neat trick is think about which greeks have the letter ‘g’ in it. There you go – that’s the long put: positive [g]amma and ve[g]a.

- And that only leaves the short put. Well that’s easy now. If the long put is positive gamma/vega then the short put must be negative gamma/vega. And of course it’s positive all the others, delta, theta, and even the mysterious rho.

You Came A Long Way

When you started reading this post the topic of option greeks may all just have been, well… ‘greek’ to you. But if you made it all the way to here then you actually understand them better than 99% of retail traders. Congratulations – you are now considered armed and dangerous by TDA and other retail option brokers. I however recommend you revisit this post every once in a while for a little refresher. In particular the impact of volatility on its other greeks is an acquired taste and either necessitates repeating or regular use. Frequent consumption of single malt Scotch may help as well – or least that’s what my local barkeep keeps telling me. Anyway, after a few weeks/months what once as dry theory should all become second nature to you.

Make no mistake – although cryptic to outsiders a deep understanding of option greeks opens up a whole new dimension of profit potential. At minimum it can keep you out of trouble ahead of or during volatile market periods; and I have an inkling we are going to see quite a bit of that in the years to come.

{kind=link}