The Wheels Are Coming Off

The Wheels Are Coming Off

Hope indeed dies last. Last Friday I stumbled across some rather silly statistics which suggested that the double digit rally last week marked the early stages of a new bull market. Such cognitive dissonance may have been caused by acute mental delirium due to late stage COVID-19, but it’s most likely related to the anticipated congressional passage of a $2 trillion stimulus bill aimed at addressing an economy that effectively has come to a screeching halt.

First up don’t believe anything you see or hear in the MSM as your average journalist knows less about the financial markets or trading than your average pet turtle. Everyone is talking about fear right now but it is confusion that currently rules markets across the board.

Just look at the SPX above which shows that it once again exceeded last week’s expected move by quite some margin. It did close nearby due to late session sell-off on Friday, but it’s become clear that markets are still doing a horrible job of pricing forward facing risk.

Massive counter rally like this are rarely good news, in fact historically they are an integral hallmark of an unfolding bear market. So if you are a perma-bear then have no fear, volatility is here to stay for quite some time to come.

Or to quote ole’ Winston: This is not the end, it is not even the beginning of the end, but perhaps it is the end of the beginning.

So the Fed released its new bail-out plan and then went all out and embarked on a spending spree of $500 Billion in the last week alone, basically snagging up anything that wasn’t nailed down. They’re buying corporate bonds, treasuries, MBS, whatever they can.

But unfortunately there is no such thing as a free lunch as the Fed’s actions are effectively changing the bond markets, most likely for a long time to come. Let me show you:

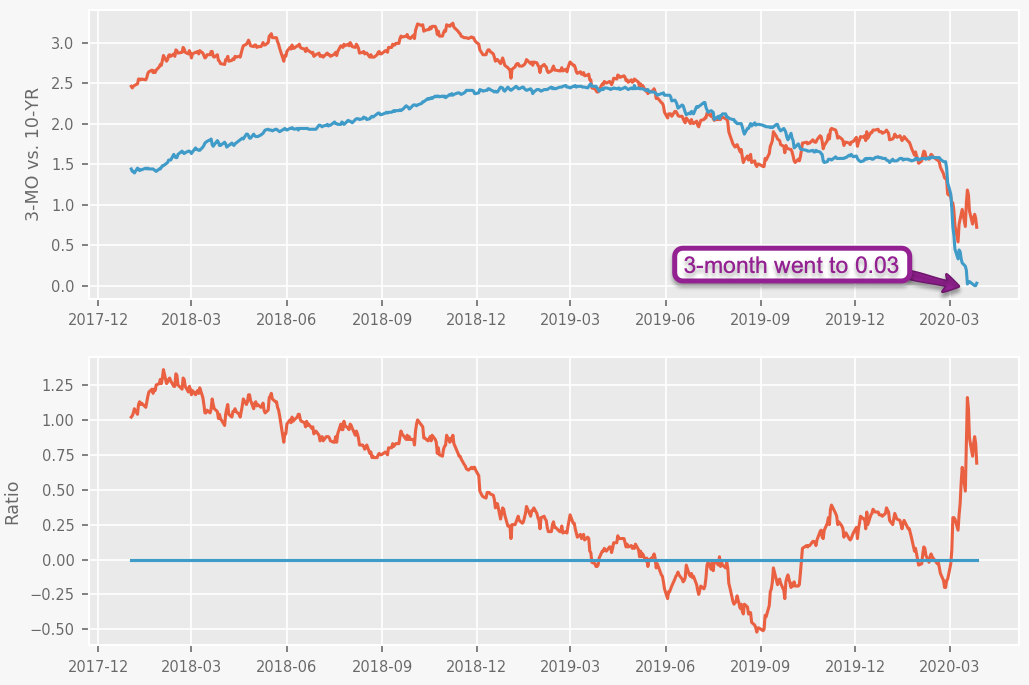

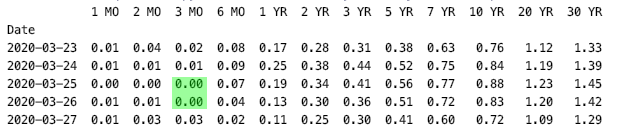

When plotting my Fed yield data I was flabbergasted to see the 3-month t-bills at a yield of 0.03%. That is until I saw the tail print of the past week:

Frankly that’s shocking. The 3-month actually bounced a little as it had been dropping to zero for two days. And what this is suggesting is that the bond market is effectively broken with only the Fed as the buyer of last resort.

BTW that’s exactly what happened in Japan and after various rounds of buying sprees it basically locked up. A few months ago I saw some articles that the Japanese 10-year (which pretty much is their bond market) stopped trading. Meaning NOBODY traded it during an entire session.

So while the Fed goes onto a buying spree the volume in the ZB slowly drops toward ZERO. Of course the Fed does not trade the ZB future contract – they trade the bonds themselves, they are active in the cash market.

What that means from a trading perspective: I would not touch this one right now. Perhaps it’s temporary and perhaps we are following Japan. Tough to say.

Fed Up or Fed Out?

The bail-out bill does not entail any clear measures as to how to where we go in the future with the economy. In 2008 it took weeks for a $900 Billion bail-out bill to be passed. In contrast the Fed literally pounced this time around and the old caricature of Bernanke tossing dollar bills from a helicopter has become reality to a certain extent.

They are buying everything they can get their sweaty hands on with a complete lack of clarity of what this will accomplish in the long term. It’s a reflexive move I think will bite us in the hind regions on a long term basis. And there is no telling if it will even work on a short term basis, at least judging by some of the gyrations the prior week when the Fed panicked and announced unlimited QE with the result that equity markets continued to drop lower.

As I keep saying over and over again: You cannot print yourself out of a demand crisis. To that effect we are going to see entire industries disappear as companies are literally hemorrhaging money right now. Some are unable to even pay rent. That’s after a 2 week lock-down. Imagine where we’ll stand three months from now.

A great reflection of global economic activity is crude oil, which dropped below the 20 mark last week. Are we going to see it at $15 or $10? Yes, very much possible. Bear in mind that the historic pain threshold for crude is $35 at which point it’s not economic to produce in many parts of the world. Shale oil most definitely comes to mind.

By the way, the next earnings seasons is going to be BRUTAL, which starts in early April – that’s a week from now!

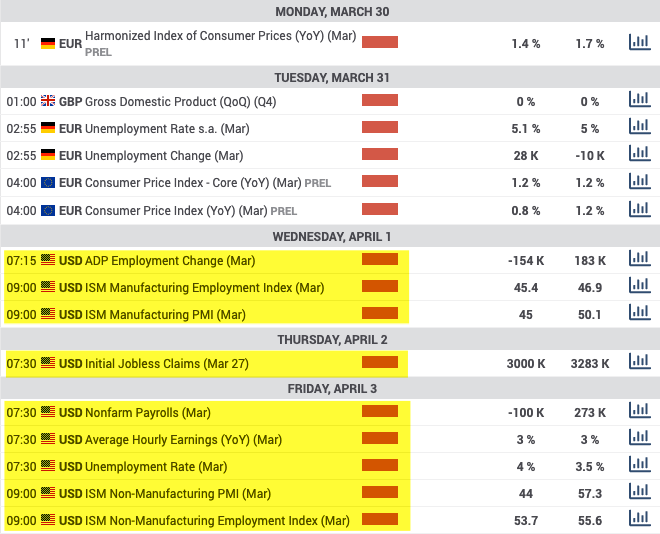

In the interim we have plenty of market movers scheduled for this week. ISM employment, Nonfarm Payrolls, ISM Manufacturing… are you not entertained??

Volatility is at historic highs comparable with what we saw during the 2008 crisis shown above. But this time around it may actually get worse than that…

It's not too late - learn how to consistently trade without worrying about the news, the clickbait, the daily drama and misinformation. If you are interested in becoming a subscriber then don't waste time and sign up here. The Zero indicator service also offers access to all Gold posts, so you actually get double the bang for your buck.

Please login or subscribe here to see the remainder of this post.