Option Basics – Debit Spreads

Option Basics – Debit Spreads

It’s Friday and thus it’s time for the third installment in our tutorial series on option theory. In the last two installments we we covered options basics and then did our best to give you a head start on how to interpret option greeks. Today we’re going to jump right into debit spreads and explain why they often may be preferable to trading naked options.

Bull Call Spread

The first strategy that we will look at is the bull call spread.

Fig.1 Bull Call Spread

To start with, I’ll give the standard definition seen in most options books or websites, as underscored by the abstract above: This spread involves buying an at-the-money (ATM) call, and selling an out-of-the-money (OTM) call, resulting in a net debit. Time is of the essence here. Maximum risk is capped at the net debit, and maximum reward is capped at the difference in strikes less the net debit. We have one break-even level — the long call strike plus the net debit.

Bear Put Spread

The bearish counterpart is the bear put spread — same type of structure, except this time you’re betting on a decline in prices. It’s composed similarly to the bull call spread but this time we’re buying and selling puts.

Fig.2 Bear Put Spread

More specifically you buy an ATM put and sell an OTM put, thus again resulting in a net debit. Maximum risk is capped at the net debit. And maximum reward is, again, equal to the difference in the two strikes less the net debit. The breakeven is the long put strike price less the net debit.

Alright now hold on. I can literally see your eyes glaze over already. In order to really develop a deeper understanding of how option strategies work it is crucial that you are grasp how two or more options interact and how they may help you to limit your risk and also increase your odds of expiring profitable.

Time Is An Option’s Enemy

Just imagine for a second you are buying an at-the-money (ATM) call. What just happened? Well, for starters you are now in a battle against time. An option by definition is a wasting asset and as such its premium will decay in value every single day, all the way into expiration. If you buy a put you are short price movement of the underlying (i.e. short delta – we cover the greeks another day) but you are still long an option and as such there’s no difference when it comes to time value (i.e. theta in the greeks). As a matter of fact it is time depletion (a.k.a. theta burn) that most option sellers rely on for profitability. They care a lot less about market direction and only to some extent about volatility.

Recall from our first installment that an option’s premium consists of two component: intrinsic value and time value. You just bought an ATM call, so the intrinsic value of that option is going to be barely above zero and over 90% of its value will be purely extrinsic (i.e. time value). Which also means unless price starts to move strongly in your direction your ATM call is going to lose a little bit of its premium every day. And that makes complete sense as an option to buy the Spiders at 200 isn’t really worth anything or much unless the Spiders are actually trading far above 200.

As you can imagine it’s even worse for OTM calls. All their value is purely time based as their premium does not contain any intrinsic value. Of course naked OTM calls have their place in trading as they are great for insurance if for example you want to hedge a short position in the underlying instrument. But buying OTM calls in anticipation of higher prices is usually a losing proposition as price would have to rise far above that call, and that soon, in order for that option to substantially increase in price.

Which is the reason why a lot of professional option traders engage in selling you those OTM calls, full well knowing that they will expire worthless most of the time. Of course that’s the rub – most of the time but not always. Sometimes, perhaps only once every few years, we see a big move that nobody expected. And that is when many naked short option sellers get taken to the woodshed. Because the biggest problem with selling naked short options is that the loss potential is unlimited. Which is the one time retail traders get to enjoy their day of glory (e.g. fall of 2008) as on the flip side their profit potential, as option buyers, is also unlimited.

But ask yourself – how often does that happen? Actually more often than even many professional traders think. There is roughly a 75% chance of one sigma 5 event per year given leptokurtic distribution models which apparently most closely resembles real world models (normal distribution vastly under estimates it by the way, which suggests only every few hundred years). The thing is this however – timing that one day per year plus minus is next to impossible. And that is what option sellers bank on.

Increase Profit Potential And Decrease Cost

There is one key consideration regarding debit spreads in that they involve limited moves. By selling an option at a strike that’s further out of the money, we technically give up certain profit potential. However, since we’re predicting that the move is limited, we’re not really giving up anything, all the while reducing cost. And actually in the vast majority of cases we are actually increasing our profit potential due to much the much reduced cost. Let’s look at an example:

A lot of guys are licking your chops about going short the S&P cash right. Admittedly we are starting to push into monthly resistance but I want to be clear that this is not spot where I would attempt to be short. However if have money to burn and would like to lock in some profits then perhaps buying puts here is not the worst idea as momentum seems to be slowing down a little.

So assuming the Spiders close around 209 today and expect the market to go down soon we’re going to look at a few possible put option scenarios. The three profit targets for all of our scenarios are going to be:

- Reasonable at 200

- Agressive at 190

- The Hail Mary at 180

I have actually had to increase the probability from 1 sigma to 2 in order to expand the odds of closing ITM even near 180. Please keep that in mind as we analyze various options and their respective profit potential.

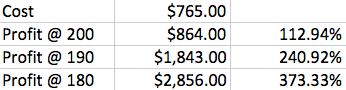

Deep ITM 216 Put Option

With the Spiders near 209 the 216P is considered a deep ITM option. You may note its vega which is currently -99.10, and that means it’s tracking the underlying ETF almost at a 1:1 ratio. Here is the possible return on your investment, which most likely underestimates an increase in vega, but at any rate:

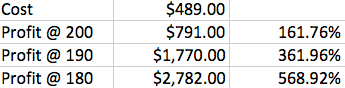

ITM 212.5 Put Option

Next we’re dropping down a few strikes to an ITM put at 212.5 with a vega of around 75. Once again here’s the profit projection:

Not too shabby, so the profit margin on the way down in pure percentage terms is increasing.

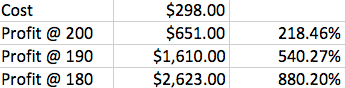

ATM 209 Put Option

Most option traders usually go for ATM options due to the lower price and as expected vega near ATM is at 0.5 which means they are going to start tracking the SPY at 50%. The profit potential:

Another reason why option buyers usually go for ATM options is the perceived profit potential. For under $300 the profit curve here looks very delicious.

Let’s Run The Numbers

But does it really? In my not so humble opinion even a drop to 200, given the bullish advance of previous weeks, probably is pretty aggressive. Odds have it that the bulls would defend the recently reconquered 2k mark on the S&P cash aggressively. So statistically speaking our profit potential starts to diminish rather quickly as we’re approaching the SPX 2k mark. And that means an ATM put costs us $289 but only gains us a little over 200%. Hey, that’s a 2R gain, which sounds great but it’s a position you’ll have to hold for almost a month and a lot can happen until then.

If you recall our lessons on system trading then you know that the lower the win/rate ratio the bigger your winners have to be just to get to break even. A significant number of long options (especially puts) expire worthless each month, which represents a 1R loss. Do you recall how to calculate the break/even point?

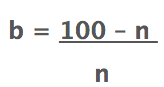

n = Success Rate in %

b = Break Even Risk to Reward Ratio

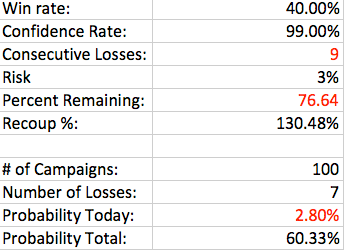

Alright, let’s be generous and say that 60% of all put options expire OTM, that would mean n (the success rate in %) equals 40. And 60 / 40 = 1.5. So just in order to break even over let’s say 100 of your put transactions you would have to bank 1.5R at minimum. I think the win/loss rate is actually lower but perhaps you’re better than most and even then you require at least 200% winners just to eek out a respectable profit of 0.5R over 100 campaigns. It’s not a bad system but let’s not forget another inconvenient fact that most option traders are oblivious to – the odds for consecutive losers:

For a win rate of only 40% the odds of experiencing 9 consecutive losers over 100 campaigns statistically speaking has a chance of about 60%. Given 250 campaigns it’s 91% and given 500 campaigns it’s 99%. Most retail traders do not abide to proper position sizing and regularly risk quite a lot more of their assets to one campaign than just the 3% I selected as 1R. And if you hit 9 consecutive losers at 3% it means you lost almost 25% of your trading capital and have to make 130% just to recoup your losses. If you trade 5% position sizes then you lost over 35% of your assets and need to make 155% to get back to where you started.

I think you are starting to get my point, which is that in order for you to make money with naked options you must a) either bank 2R winners on average or b) increase your win rate substantially above 40%. You think you can do that?

Naked Options Are Honey Traps

And this exactly the honey trap that newbies tend to fall into. You want cheap options with outlandish returns, but in reality, this unlimited return will happen only very rarely (e.g. 1 out of 100 times). You know how this goes and I’m sure you’ve been there yourself in the past. You pick up an ATM option with an intention of making a quick money, but the moment you get in, the market starts to go against you. You don’t want to get out of the position until you break even, so you decide to hold on to your position.

A couple of weeks passed by, and SPY comes back to your entry price. In the meantime, you’ve lost a ton of money on a time decay and wind up getting out of your position with a loss, instead of taking an “unlimited” gain. So, while I’m not totally discarding naked puts as a strategy, I think in most cases there is a better long term approach which may not bag you the 10-fers you dream of but put you on the path to banking consistent coin via a systemic approach that clearly defines a win/loss range and is less sensitive to theta burn or gyrations in vega (topics we have not even discussed in the context of naked options).

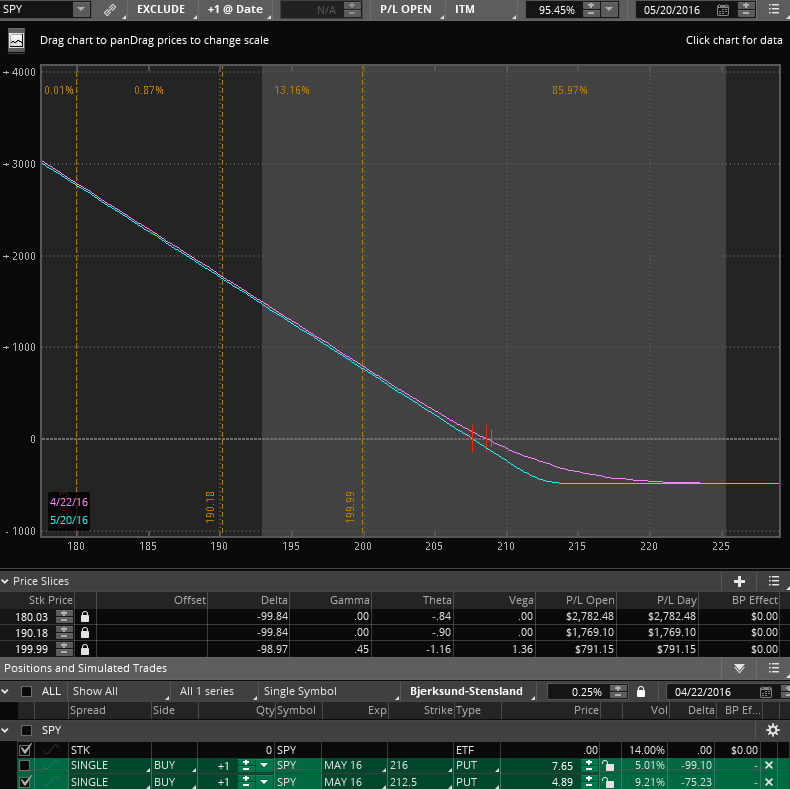

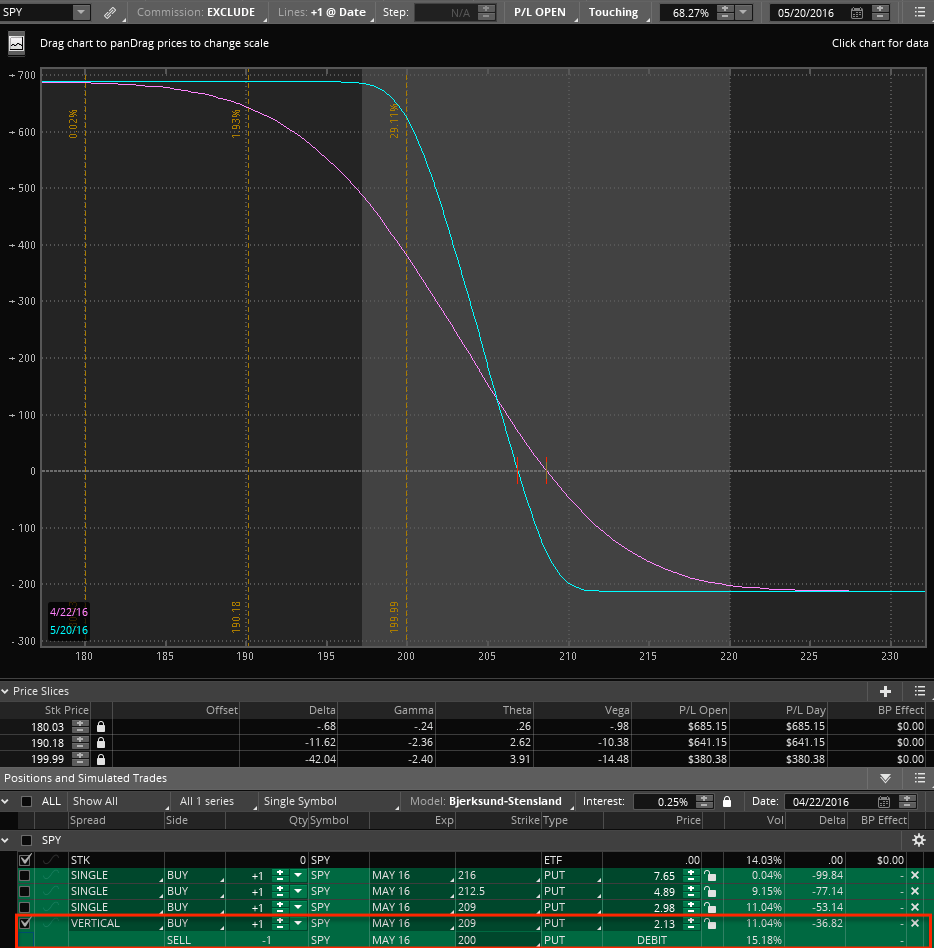

209/200 Vertical Put Spread

So what we’re doing here is to buy a put at 209 and at the same time sell one at 200, which establishes a debit spread. The cost of this campaign is 2.13 which is lower than that of a naked ATM put. So that alone reduces your cost of entry and especially if you have a smaller trading account allows for more precise position sizing. If you want have a $100k account and only want to risk 1% (advisable) on this then you would be able to 9 of those suckers.

On the ROI projection we see that getting to the 200 mark nets you a little under 180%. Yes, that’s less than for the naked put but remember that after about 205 time decay (i.e. theta) actually starts helping instead of hurting you. The longer it takes to get to 200 the more you make on theta. It is true that a rise in volatility will hurt you a little but unless you timed your purchase perfectly a lot of that is most likely offset by the lack of theta burn. Only an almost instantaneous drop would make a naked option the right choice here. So if you have a crystal ball at home then that’s most definitely the way to go 😉

How To Pick Your Strikes

You’d be surprised to learn that most professional option traders rarely glance at a chart. Well, at least not the type of chart you are used to looking at. Instead they look at what’s going on in the option chain, so let’s see what’s going there:

And here it is – we’ve got the calls on the left and the puts on the right. Now look at the open interest columns. Despite current bullish tape we’re seeing some pretty significant activity around the 205P and the 200P. So quite a lot of market participants seem to be putting money on a bet that prices will drop toward either 205 or 200 in the next month. That is quite an aggressive assessment if you ask me, especially given all we learned about theta burn in the last month of an option’s lifetime.

But without even looking at a chart you are able to get a pretty good assessment of price levels that market participants perceive as being significant. If you can line them up with technical support levels on your charts then even better. However given the lack in technical context on my own charts, meaning according to my personal lens of the market, I must conclude that even a vertical put spread right now right here has only limited odds. In addition I don’t see too much clustering on the put side of the option chain. It’s understandable that we have a more significant OI around the 200 mark but it’s only about 150k and that’s not a hell of a lot. There is barely anything around 201 or 202 and that IMO is a bit suspect and suggests that the 140k is mostly composed of retail traders.

Realistic Expectations

What have we learned today? First of all before even thinking about trading naked options or directional strategies such as vertical spreads we should make a realistic assessment of the current trading environment. What are the odds of a reversal and how deep do you expect this reversal to be? What is your conservative/moderate/aggressive price targets?

We have also learned that buying options in general has a low win/loss rate and that a significant number of them expire worthless. That in turn affects our minimum win/loss rate and as such we need to increase our odds of success as much as possible. Unlike being long in the futures or forex markets buying options puts us into a race against time. And that means our position loses money every single day in sideways tape. A vertical spread keeps us out of the time race and actually helps us assuming that prices move at least somewhat in the direction of our price targets. Which may allow you to get out at or near break/even should market behavior indicate that the odds of reaching your target are diminishing. So in other words choosing vertical spreads instead of naked options offers you more flexibility as market conditions change.

Trading A System Of Options

Finally from a purely systematic perspective vertical spreads allow us to more precisely evaluate our benefit to risk ratio. It’s just not realistic to think in terms of ‘open ended’ returns – when trading any systems, options included, you must know what your targets are. Without profit targets you don’t know when to exit your campaign and one of our prime directives here at Evil Speculator is that you never enter a trade without knowing where/when you will exit it. If you choose for example to take partial profits at 2R and keep the rest until 3R then that is a system you can factor and statistically analyze over time. Which will allow you to track your win/loss rate, your average expectation (or SQN), your standard deviation, your consecutive losses/wins, average loss vs. average win, etc. etc. Which are topics I almost never see addressed when it comes to trading options. It is quite possible to trade a system of options instead of just trading options. The difference between the two is profound and we will spend quite a of time on this in the weeks and months to come.