The Road To Hell

The Road To Hell

The biggest news yesterday was not that the Fed once again chickened out and left the federal funds rates untouched at zero. I could have told you that ahead of time. And guess what – I actually did on several occasions. No, real big shocker yesterday was some very carefully worded mention of negative interest rates. Say what? The sheer fact that these three words were uttered by Mrs. Yellen during her address speaks bounds about the growing fear deep inside the bowels of 33 Liberty St.

Who of us would have thought a year ago that we would be entertaining the thought of NIRP instead of raising interest rates perhaps for the second or third time by now? And that exactly is the crux of the matter isn’t it? There is absolutely no predicting as to what Fed will do next as its actions appear to be not only reactive but also fearful of causing a market dislocation years after resorting to ZIRP.

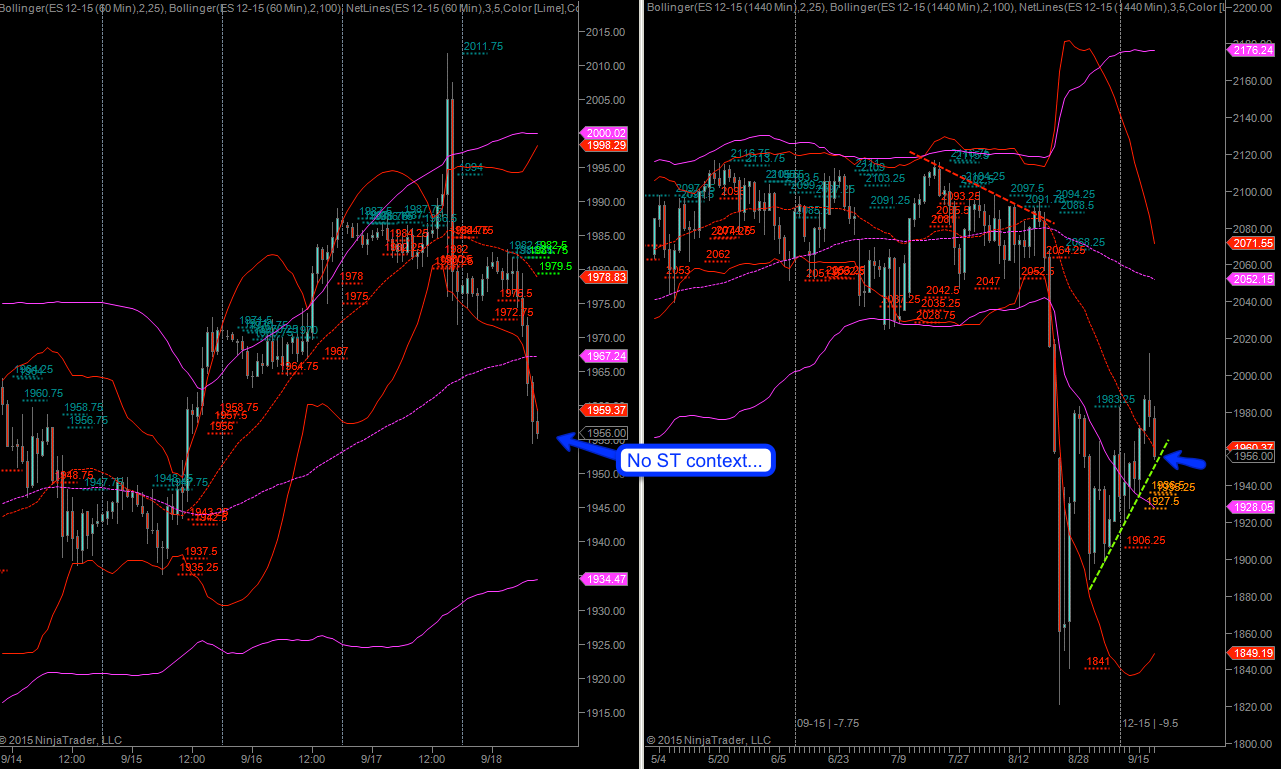

The big paradox however is that this is exactly what we may be getting. Had the Fed been crystal clear about the possibility of NIRP to begin with then it would have been part of the equation for investors and traders like us. And I’m not saying all this to complain – rather it’s to make a very important point. Clearly market participants are throwing in the towel here as confusion now reigns high. Overnight equity futures across the board have sold off heavily and one wonders if the speculators are now taunting Mrs. Yellen to cross the Rubicon and bring about NIRP.

You may have heard the old saying: The road to hell is paved with good intentions. The deeper meaning of which is that a series of well meant decisions can sometimes put you on the path of accomplishing the exact opposite of what you set out to do to begin with. By mention of NIRP during a time when an interest rate hike was on the roster the Fed now has clearly signaled that it is afraid of a major market dislocation. Whether or not we will ever see NIRP is beside the point here. What matters is that we should continue to expect seeing the level of intra-day volatility we all have come to enjoy so much over the past year. And as traders that affects our daily reality quite profoundly. At minimum it means wider stops, smaller position sizing (those two usually go hand in hand), different campaign management (e.g. closer trail), and very stringent capital commitment guidelines (e.g. correlations, markets, etc.).

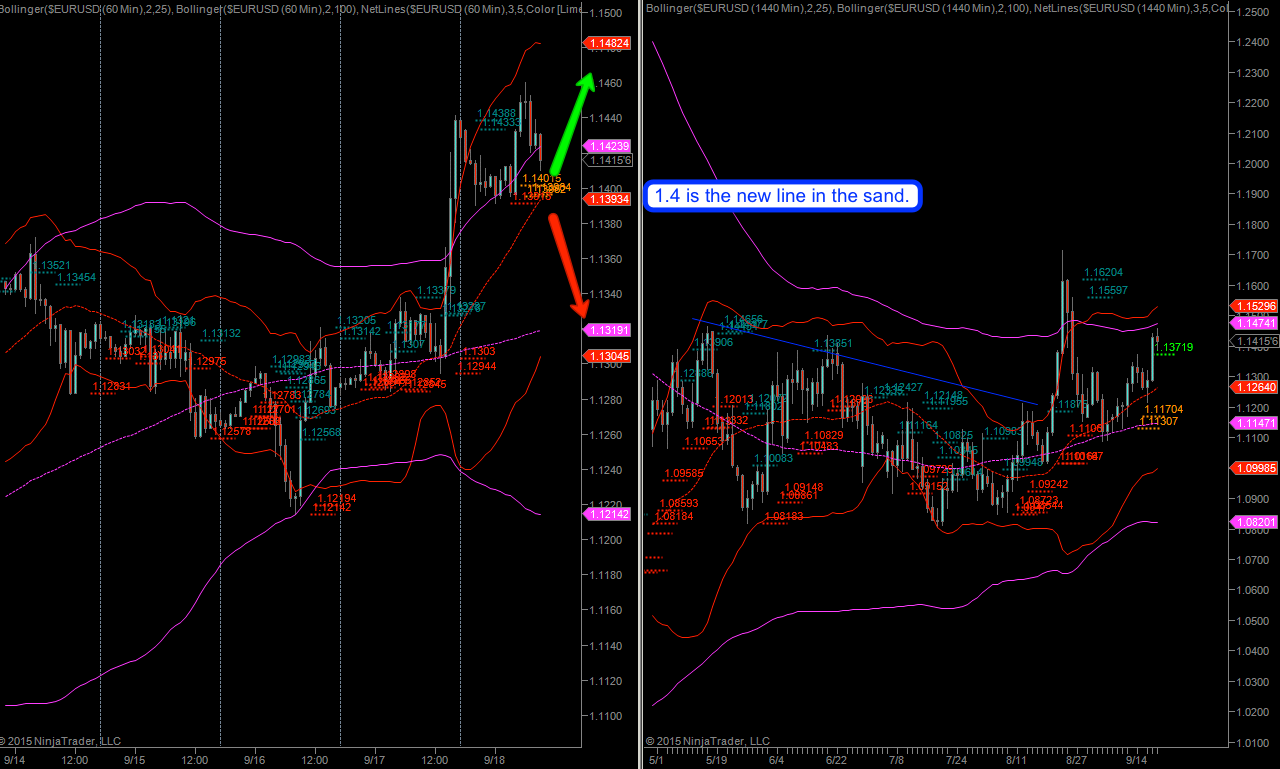

On to the setups: The EUR/USD is a possible long while it’s hovering near 1.4. In my mind that has been a long time coming and unless we hear some jawboning by Mr. Draghi in the near future I thing my days of enjoying a favorable exchange rate may have come to an end now. Just looking at the daily panel screams short squeeze to me. Of course the ECB could smash this chart in a heartbeat but thus far I have not seen/heard anything.

If we drop below 1.4 I’ll try to ride it lower back to the 100-hour SMA. But that one thus far has served as support quite well, and if that one gives I think the 25-day SMA is where the Euro specs will once again make their stand.

A few more goodies below the fold:

It's not too late - learn how to consistently trade without worrying about the news, the clickbait, the daily drama and misinformation. If you are interested in becoming a subscriber then don't waste time and sign up here. The Zero indicator service also offers access to all Gold posts, so you actually get double the bang for your buck.

Please login or subscribe here to see the remainder of this post.

Cheers,