The New Old Normal

The New Old Normal

Implied volatility has been dropping faster than an ACME anvil over the past two weeks, which stands in stark contrast to what I am seeing in the bonds market so the jury is still out whether or not we are looking at some bifurcation here (strange things happen sometimes) or if risk is being improperly handicapped. If it is the latter then we may see another Gamestop type situation unfold in the near term future – if it’s the former then retail traders are about to get a wedgie of biblical proportions.

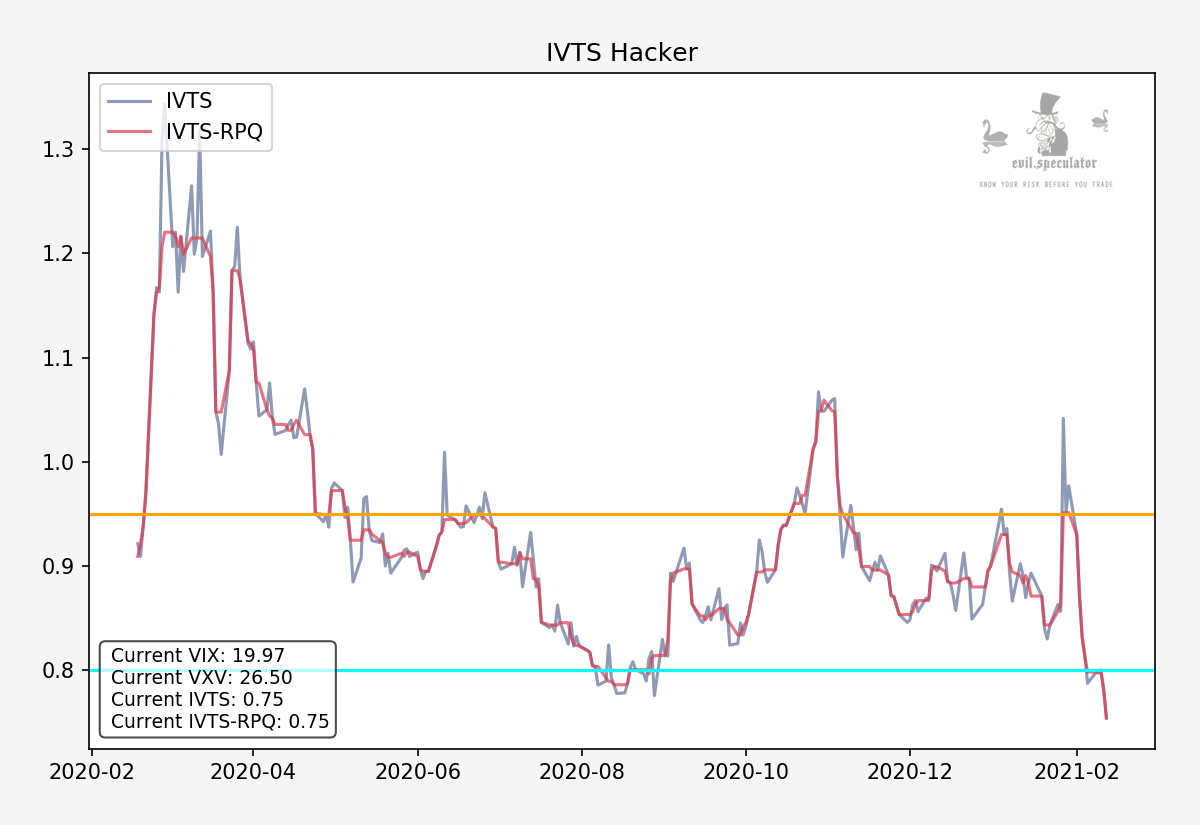

On the surface everything is looking pretty hunky dory with the VIX back to pre-COVID levels, albeit the 20 mark has yet to be decisively cleared (there as a dip below it on Friday).

The implied volatility term structure is also in a quick dive pattern and I honestly cannot remember the last time I’ve seen this ratio at the 0.75 mark – it’s been at least a year.

But if you look closer you start seeing the first cracks in the armor. Note that the VIX is now near 20 with the VIX3M (formerly VXV) still all the way up at 26.5.

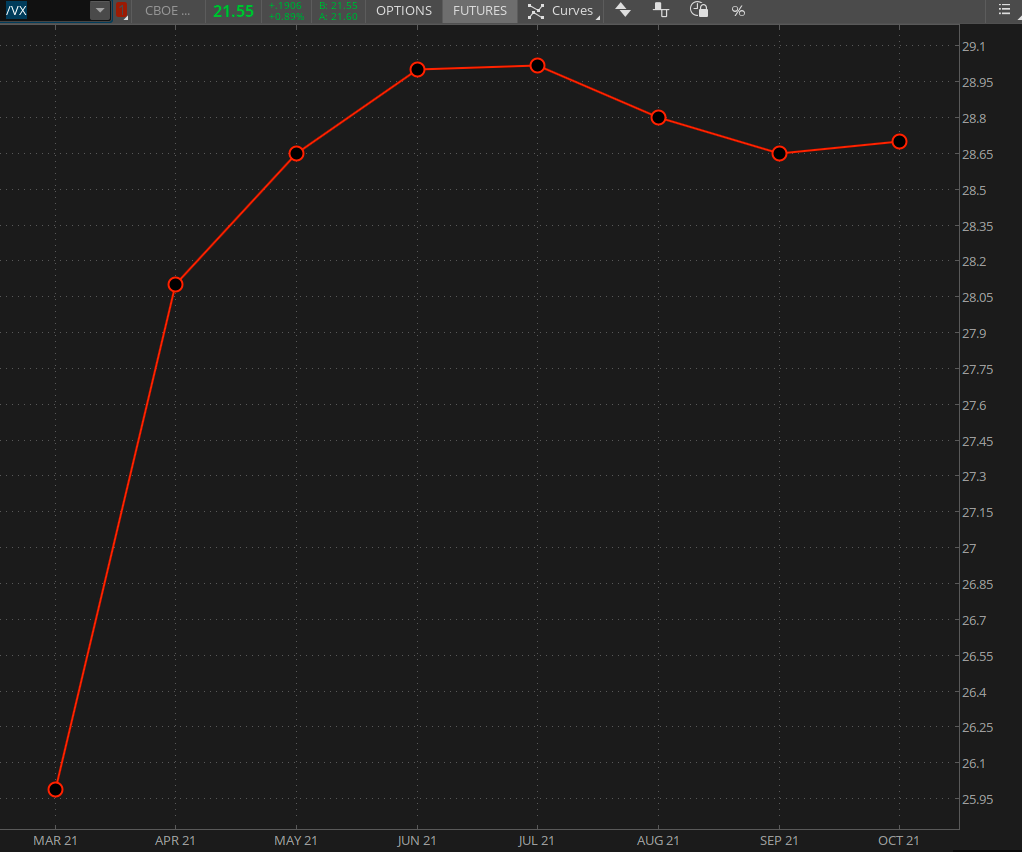

And that’s where things start to get really interesting. If you take a peek at the VX product depth graph then you’ll see even higher prices for VX contracts further out toward the summer. And excessive contango in the VX futures usually is the harbinger of tough times ahead.

Because according to my stats it is in fact retail that’s gobbling up VIX related positions (mostly in related ETFs like VXX or UVXY). And yes albeit it’s possible that retail has it right and the evil quants and market makers (paging HD) have it all wrong this is giving me a lot of pause.

Especially if you consider this:

It's not too late - learn how to consistently trade without worrying about the news, the clickbait, the daily drama and misinformation. If you are interested in becoming a subscriber then don't waste time and sign up here. The Zero indicator service also offers access to all Gold posts, so you actually get double the bang for your buck.

Please login or subscribe here to see the remainder of this post.