OPX Once Again!

OPX Once Again!

(Doesn’t the above Mt. Fuji look like a calendar spread??)

Fujisan here.

I had such a wonderful week. Boy, I love OPX!

I was able to nail three major tech companies, namely, GOOG, AAPL, and RIMM, this OPX week. If you look at my posting on June 11th at https://evilspeculator.com/?p=8316, you can see how I picked up my GOOG and AAPL trades. I picked up GOOG 400/410/420/430 condor with a target price of 415, and AAPL 30/35/40 butterfly with a target price of 37.5 I did very well on these trades – I had a 200% return on GOOG and a 100% return on AAPL, not to mention my various SPY calendar/condor positions.

RIMM Double Calendar Spread

RIMM had an earning release on Thursday evening and many of you picked up RIMM’s earnings play. You might have gone bullish, or bearish, but I decided to go neutral with 75/80 double calendar for IV play.

What is IV play?

If you look at my first option post on April 4th at https://evilspeculator.com/?p=5897, I discussed the concept of IV rush. What happens right before earnings is that, MM pumps up IV (Implied Volatility) to inflate the front month option premiums. In RIMM’s case, front month IV was as high as 190% (June 80 call), which dropped down to 67% by the time I cashed it out.

With ATM calendar spread, you can make money on IV crush as long as the underlying stays within one standard deviation. You are working with high probabilities and a success ratio of this option strategy is very high on earnings.

I posted this PL graph in last April when RIMM had an earnings in Q1. Here is what RIMM’s ATM straddle looked like before earnings:

Here is a look after earnings:

Do you see a big plunge in ATM straddle? This is because of IV crush after the earnings, and this is exactly the reason why people lose money on earnings play.

Two things have to happen in order to make money on earnings; that is,

1. You have to pick the right direction, and

2. The underlying has to move more than one standard deviation just to break even (which is 32% probabilities) for you to make up for inflated option premiums you have paid for right before earnings.

3. If the stock didn’t move more than one standard deviation, you will lose money (which is 68% probabilities)

Now, let’s look at ATM calendar that I have put on for RIMM on Thursday.

(Note: The reason that I picked up 75/80 double calendar is because RIMM was trading between 75 and 80 on Thursday and I wanted to have a delta neutral position).

After earnings:

The total cost of this trade was $4.48 to make $1.4 and the risk/reward was 31%. This is not bad at all for one day trade.

Here is a summary of the ATM calendar trades from last Q1 earnings that I posted on April 18 at https://evilspeculator.com/?p=6308. The whole concept of trading ATM calendar is to capture IV crush and the average trading results so far is 35%

This strategy is by no means going after a home run, but I have a high success rate on this trade (so far, 100% winning ratio), and this is definitely something to consider when you pick up earnings play next time. Going after a home run hardly pays off and, sadly, it never happened to me in my trading career.

June Quarter OPX

Yes, believe it or not, we have another OPX coming up in one more week, and this is a great time to plan for another OPX play. This OPX only includes major indices and ETFs.

I saw some of you making a “pin” play during OPX week, but I would rather put the positions at least 5 days prior to OPX and then wait for the market to come in to hit the short strikes. This way, I would have plenty of time to adjust my positions and it would be a much better risk/reward.

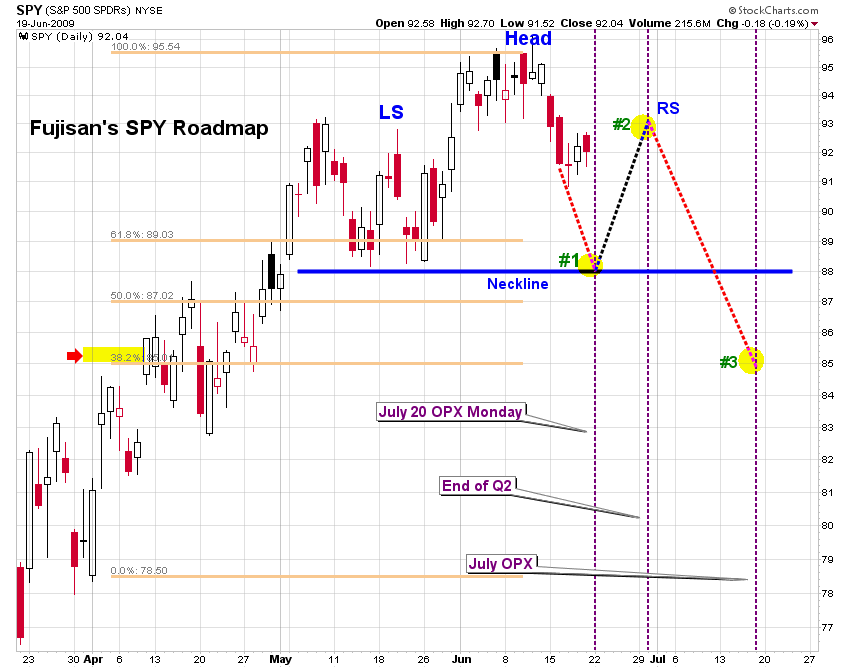

Now, Doula has put together a nice chart for me, so I decided to use her chart (thanks, Doula!). The time frame may be a little bit off, but this is what I’m looking for right now — a H&S pattern.

As soon as SPY comes down to 88 level to test a neckline and if it holds, I am going to start putting together mildly bullish June Q butterfly/calendar positions as I’m expecting a retracement toward the end of June for a window dressing.

Just by looking at June Q open interests, it looks like SPY 90 and 92 have the most interests (besides 86), so this is where I would be shooting for by probably putting together 92 calendar, 88/92/96 butterfly, or 88/90/92/94 condor. Open interests are not accurate measurement by all means, but at least give me some guidance as a good market expectation.

These are just some ideas based on the information that I have now. This could be changed significantly next week, depending upon how fast and how deep the market comes down. Please modify the position as you find it more appropriate to your risk tolerance.

Here is an example of 92 JuneQ/July calendar spread.

SPY 88/90/92/94 Condor.

Lastly, my favorite butterfly – 88/92/96.

Again, these are just ideas of taking advantage of another quarter-end OPX. Please plan ahead your position, know when to make an adjustment and when to get out. But, most importantly, have fun with it!

Issac Asimov vs. Elliotte Wave

Lastly…. growing up in a small town in Japan, I used to have such an admiration for American culture. I listened to American pop music and read American novels. Especially, I was a big fan of science fiction. Among them all, I loved “Foundation Series” written by Issac Asimov. Imagine Japanese teenage girl reading Issac Asimov’s Foundation series?? You can tell that I was not an average Japanese teenager, but I thought that it was such a fascinating story — you can predict a future by using “psychohistory”…..

More than a decade later when I was first introduced to EW theory, I learned that Asimov’s foundation series was based on Socioeconomics (which was named way after he wrote his first series of Foundation), everything came togehter and I felt like I found a last piece of the puzzle that I was looking for, and it explained why I was so fascinated by EW theory right away. I have already known many years ago that this would happen to me. Life is so fascinating.

Have a good weekend, everyone.

Fujisan.

{kind=link}